1. Introduction

Since the beginning of the new century, China’s economy has entered a stage of rapid development. Correspondingly, China’s carbon emissions are also growing faster than the other countries in the world. As a responsible country, China has made many commitments in the international arena that it will make its own efforts to decrease carbon emissions to contribute to the environment.

Zheng’s analysis outlines the challenges and opportunities China faces in addressing climate change after the 2009 Copenhagen Climate Change Conference. The author presents several strategies for China to combat climate change, such as prioritizing energy conservation, enhancing efficiency, and fostering renewable energy development [1]. Mallapaty underscores the significance of China’s commitment to carbon neutrality and the pressing global need for action to tackle the climate crisis. The authors emphasize the importance of policy measures and technological innovations in achieving carbon neutrality, alongside the necessity for substantial investments in renewable energy and grid infrastructure. They also point out that China’s leadership in renewable energy deployment and CCUS technology can serve as a model for other countries to emulate, with continuous cooperation and collaboration essential for global emission reductions [2].

Chen’s analysis explores China’s potential for leading in the global transition to a low-carbon economy, particularly through the Belt and Road Initiative, which presents opportunities for renewable energy development and technology transfer. The author discusses China’s commitment to achieving carbon neutrality by 2060 and highlights policy measures such as carbon pricing, renewable energy incentives, and energy efficiency standards. Additionally, the author delves into China’s technological innovations in carbon capture, utilization, and storage (CCUS), as well as hydrogen [3]. Sun and Chen assess the impact of green finance on China’s regional energy consumption structure, noting that it has driven China’s shift to clean energy, especially in more developed regions. They suggest that policy interventions, like feed-in tariffs and renewable portfolio standards, could further accelerate this transition while emphasizing the importance of green finance in propelling China’s transition to a more sustainable energy consumption structure [4].

Jiayu, B. et al. highlight that China has become the world’s largest producer and consumer of renewable energy, boasting a total installed capacity of 896.39 GW by the end of 2020. They also note that solar and wind energy are China’s fastest-growing renewable energy sources, with respective installed capacities of 253.43 GW and 281.51 GW. Concurrently, the authors identify challenges facing China’s renewable energy development, such as the intermittent nature of renewable energy, inadequate infrastructure, and high costs of renewable energy technologies. They propose several measures to promote renewable energy development, including increased government support, integration of renewable energy into the grid, international cooperation, and improved public awareness and education. If implemented effectively, these measures could help China continue its transition toward a more sustainable and renewable energy future [5].

Muradov and Veziroglu argue that transitioning from a fossil-based economy to a hydrogen economy is crucial for reducing greenhouse gas emissions and combating climate change. They review various carbon-neutral technologies, including biohydrogen, solar, wind, and nuclear hydrogen. The authors suggest integrating renewable energy into the energy system is necessary to enhance the overall efficiency of hydrogen production and reduce the carbon footprint of hydrogen-based technologies [6]. Xie et al. use Anhui Province as a case study to examine the carbon emission reduction potential of different coal regulatory scenarios, such as coal consumption caps, coal-fired power plant closures, and a combination of both. They assess coal regulation’s health and environmental co-benefits by quantifying reductions in air pollutants, including sulfur dioxide, nitrogen oxides, and fine particulate matter. The authors find that combining coal consumption caps and power plant closures is the most effective way to reduce carbon emissions. Coal regulation significantly reduces air pollution levels and associated health risks and the greatest benefit resulting from the closure of coal-fired power plants [7].

Recognizing the significant share of the building sector in global energy consumption and carbon emissions, Zhang et al. explore its importance in achieving carbon neutrality. They outline China’s current building energy consumption and emissions, noting that buildings account for 28% of China’s total energy consumption and 25% of its carbon emissions. The authors discuss the development of China’s Near-Zero Energy Building (nZEB) standard, which aims to reduce building energy consumption and emissions through improved insulation, ventilation, lighting, and renewable energy technologies. The potential of implementing the nZEB standard can help China achieve its carbon neutrality goals [8].

Shi et al. find that a low-carbon transition would yield positive societal impacts, such as enhanced public health due to reduced air pollution. However, they acknowledge that the transition could also lead to job losses in certain industries, like coal mining and refining. The authors suggest that policy interventions, such as reskilling programs and social safety nets, may be needed to help workers in these industries transition to new jobs. In the energy sector, they discover that the low-carbon transition will result in a shift toward renewable energy sources, such as wind and solar. They also note that the transition may require investments in energy storage and grid infrastructure to accommodate the intermittency of renewables. Additionally, the authors examine the potential economic costs of the low-carbon transition, concluding that while short-term costs, such as investments in new infrastructure and technology, may be incurred, the long-term benefits of reducing greenhouse gas emissions and improving public health could outweigh these costs [9].

2. Carbon Neutrality Development in China

2009-2013: The nascent stage of China’s carbon-neutral market involved pilot projects in select cities and provinces to evaluate carbon trading mechanisms. Notably, China launched its first carbon trading platform in Shenzhen in 2013, with 635 of the city’s most prominent emitters participating in a voluntary emissions trading scheme. Concurrently, the government initiated the creation of a regulatory framework to bolster the growth of the carbon-neutral market, which included the establishment of a national carbon registry and the introduction of national carbon emission standards.

2014-2017: In 2014, the Chinese government unveiled a nationwide carbon trading scheme encompassing all major industries, such as power generation, steel, cement, and chemicals. The program aimed to foster a market-based mechanism that would encourage companies to reduce carbon emissions, subsequently decreasing China’s overall carbon intensity by 40-45% by 2020. Initially piloted in seven provinces and cities, the scheme was extended to cover the entire country in 2017. During this period, the government also introduced a range of policies to support the growth of the carbon-neutral market, including tax breaks for renewable energy investments and establishing a green development fund for financing low-carbon projects.

2018-2020: China’s carbon-neutral market flourished, becoming the world’s largest carbon market by trading volume in 2019. The government continued refining the regulatory framework, including introducing a national carbon pricing system that established a price for carbon emissions and penalties for companies exceeding their emissions targets. Additionally, the government announced ambitious targets for renewable energy, planning to increase the share of non-fossil fuels in the country’s primary energy consumption to 15% by 2020 and 20% by 2030.

2021-present: In September 2020, President Xi Jinping announced China’s commitment to achieving carbon neutrality by 2060, which spurred the development of a carbon-neutral market in the country. Subsequently, the government launched policies to support this goal, including the establishment of a national carbon trading market that covers more than 2,200 power companies and other major emitters. Expected to be the world’s largest carbon trading scheme once fully operational, this market will likely help China achieve peak carbon emissions by 2030. Additionally, the government has unveiled plans to increase the share of non-fossil fuels in the country’s energy mix to 25% by 2030 and peak coal consumption by 2025.

China has made substantial strides in developing new energy sources, with renewable energy accounting for 16.1% of the country’s total energy consumption in 2020 (National Energy Administration, 2021). The country has become the world’s largest producer and consumer of renewable energy, boasting a total installed capacity of 895 GW, representing more than 30% of the global total (International Energy Agency, 2020).

Solar Energy: China, the world’s leading solar energy producer, had a total installed capacity of 253 GW in 2020 (International Energy Agency, 2020). The country has significantly reduced solar energy costs, with solar power prices decreasing by over 80% since 2010 (International Renewable Energy Agency, 2020). China’s government supports solar energy development through policies such as feed-in tariff systems and the promotion of distributed generation (National Development and Reform Commission, 2021).

Wind Energy: As the world’s largest wind energy producer, China’s total installed capacity reached 281 GW in 2020 (International Energy Agency, 2020). The government supports wind energy development through policies like feed-in tariff systems and the promotion of distributed generation (National Development and Reform Commission, 2021). Furthermore, China has made considerable progress in offshore wind energy, aiming to achieve a total installed capacity of 40 GW by 2025 (China Daily, 2021).

Hydro Energy: China, the world’s leading hydro energy producer, had a total installed capacity of 356 GW in 2020 (International Energy Agency, 2020). The government supports hydro energy development through policies such as promoting small and medium-sized hydropower projects and developing pumped storage hydropower (National Development and Reform Commission, 2021).

Energy Storage: China has also made significant progress in developing energy storage technologies, with a total installed capacity of 51.4 GW in 2020 (National Energy Administration, 2021). The government supports the development of energy storage through policies like establishing pilot projects for energy storage systems and promoting the integration of energy storage into the power grid (National Development and Reform Commission, 2021).

In summary, China has made remarkable progress in its pursuit of carbon neutrality, with significant advancements in renewable energy and a comprehensive, evolving regulatory framework. As the world’s largest producer and consumer of renewable energy, China is poised to play a pivotal role in the global transition toward a carbon-neutral future.

3. Potential Impacts of Carbon Neutrality on the Chinese Economy

The transition to carbon neutrality offers numerous benefits for the Chinese economy. Firstly, adopting renewable energy sources such as wind, solar, and hydro will foster new industries and create job opportunities. The renewable energy sector has already generated over 10 million jobs in China, a number that is expected to grow as the country moves towards carbon neutrality (International Renewable Energy Agency, 2020). Secondly, decreased fossil fuel consumption will reduce China’s reliance on imported oil, gas, and coal, thereby enhancing the nation’s energy security. Thirdly, implementing energy-efficient technologies and practices will lower energy costs for businesses and households, increasing disposable income and stimulating domestic consumption.

However, achieving carbon neutrality also presents several challenges for the Chinese economy. Firstly, the high costs associated with transitioning to renewable energy sources and adopting energy-efficient technologies may slow economic growth. Secondly, the downturn of the coal industry, which currently employs millions of workers, could lead to social and economic issues, particularly in regions heavily reliant on coal. Thirdly, the shift to renewable energy sources necessitates substantial infrastructure investments, potentially burdening public finances.

Despite these challenges, the pursuit of carbon neutrality offers several opportunities for the Chinese economy. Firstly, the development of renewable energy sources and energy-efficient technologies will generate new markets and industries, promoting innovation and stimulating economic growth. Secondly, transitioning to carbon neutrality will bolster China’s image and reputation as a responsible global player, potentially attracting more foreign investment and enhancing the country’s soft power. Thirdly, the advancement of renewable energy sources and energy-efficient technologies will support China in meeting its air pollution reduction targets, leading to improved public health and lower healthcare costs.

To fully capitalize on the benefits of transitioning to carbon neutrality and to mitigate its challenges, the Chinese government should implement policies that promote the development of renewable energy sources and energy-efficient technologies. Such policies could include financial incentives for renewable energy projects, subsidies for energy-efficient technologies, and regulations that encourage energy conservation and efficiency. Additionally, the government should invest in infrastructure and research and development to expedite the adoption of renewable energy sources and energy-efficient technologies.

The move towards carbon neutrality will substantially impact the Chinese economy. While it brings challenges, such as high costs and socio-economic issues, it also offers opportunities like developing new industries and enhancing China’s image and reputation. By implementing policies that support the growth of renewable energy sources and energy-efficient technologies, the Chinese government can fully realize the benefits of carbon neutrality while ensuring sustainable economic growth and social stability.

4. Outlook on Economic Impact and Investment Value

4.1. New Energy Resources

With the aim of achieving peak carbon emission by 2035 and carbon neutrality by 2060, new energy resources such as solar energy, wind energy, and hydro energy are growing rapidly. If China can get the upper hand in that respect, it would be able to specify the relevant standards and control the voice, which will help China make more money on that. Today, with the progress of new technologies, the cost of new energy has begun to decline significantly and started to converge with traditional fossil energy. Compared with traditional power generation technology, new energy has great advantages in the marginal cost of power generation. The Western regions, which are rich in energy resources, have the advantage of low-cost photovoltaic power generation. Through the transmission of ultra-high voltage technology and the application of intelligent micro-grid technology and energy storage technology, it could achieve the aim that the cost of clean energy be lower than that of the cost of traditional power.

To a great extent, the development of new energy requires a large amount of capital and resources, which is indispensable from government support and investment. At the same time, the marketization degree also needs support from the investors. China now has fully entered a stage of development at parity without subsidies as a result of having a fully developed new energy industrial chain and dropping new energy development and construction costs, realizing the shift from a market-driven to a subsidy-driven economy. With the acceleration of the construction of large-scale wind power, photovoltaic base and rooftop distributed photovoltaic development in desert and Gobi areas, the investment in new energy is obviously accelerating. New technologies, such as the increased efficiency of photovoltaic modules and the increasing production of wind turbines, have provided a more convenient and efficient means of the utilization of new energy resources.

4.2. Energy Storage

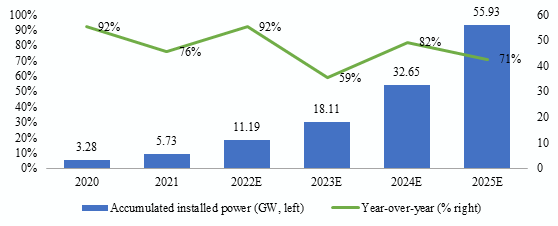

Since the carbon targets are confirmed in China, many provinces have introduced policies to encourage and force power generation side storage distribution. In order to drive the installed capacity growth, China has changed to market-oriented shared energy storage from mandatory storage. In 2022, all the provinces in China introduced the 14th Five-Year energy plan, and the scale that has been announced has surpassed 40GW in total [10]. It is estimated by the year 2025, it will reach 55.93 GW.

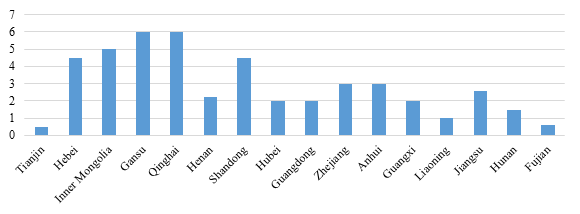

Fig.1 shows the storage plan of 16 provinces in China.

Figure 1: China’s 16 provinces of the 14th five-year plan for new energy storage (GW).

As can be seen from Fig.1, Gansu and Qinghai rank the highest among all the 16 provinces, the storage of which has reached 6 GW [10]. This is high because Gansu and Qinghai are important new energy base in China, which has formed the maximum boost force of power side energy storage. Following Gansu and Qinghai, provinces like Hebei, Inner Mongolia and Shandong also have great energy storage potential. Comparatively, Tianjin and Fujian rank the lowest. As the energy storage target is becoming gradually clear in China, the development of energy storage in the next years is highly certain.

As Fig. 2 shows, by the year 2025, China’s newly accumulated installed energy storage power will reach 55.93 GW [10]. It can be seen that China’s power generation side storage is increasing year by year, which shows that the supporting role of the energy transition has initially emerged.

Figure 2: China’s accumulated installed power of new energy storage in 2020-2025E.

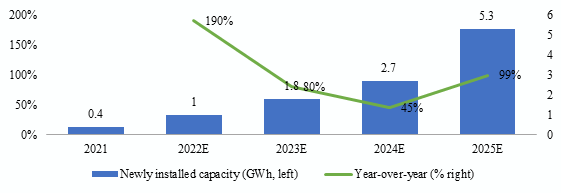

In regard to industrial and commercial energy storage, China has adjusted its time-of-use tariff policy within more than 20 provinces, trying to widen the peak price gap level and establish the peak tariff mechanism so as to encourage industrial and commercial users to configure energy storage. At present, the revenue of China’s industrial and commercial energy storage mainly comes from two aspects, and one aspect is from peak arbitrage, which is the majority of commercial and industrial storage revenues. The other part comes from the surplus capacity, which can participate in the auxiliary power market bidding to provide service for those who need it. It is expected that China’s domestic industry and commercial energy storage will move into the fast lane under the policy of tightening power rationing and the promotion of market-oriented electricity prices. As can be seen in Fig. 3, the newly accumulated energy on the industrial and commercial side has increased from 0.4 GWh to 5.3 GWh [10].

Figure 3: 2021-2025E China’s industrial and commercial industry energy storage capacity (GWh).

With the deepening of the market-oriented reform process of electricity, the adjustment of the energy structure based on renewable energy is continually promoting the expansion of energy storage. Users are also engaging in flexible demand responses at the same time. Unlike other technologies, user-side energy storage is direct to the user, and the scale is relatively small and can be controlled autonomously. At present, user-side energy storage in China is just starting. The benefits of user-side energy storage are affected by various aspects, such as investment cost and peak difference. In general, energy storage batteries have high costs and a long return on investment cycle, and the cost is usually hard to recover.

Energy storage has profoundly changed the way electricity is produced and consumed, and it has a vast market space. With energy storage having wider applications and reduced costs, China’s energy storage market will eventually mature, and the future prospects will be very optimistic, which is beneficial for achieving the aims of a carbon-neutral plan in the final end.

4.3. Imports (Coal and Lithium, Price Trend and Volume)

Since the new energy industry plays a key role in achieving the goals of the double carbon aims, energy imports such as coal and lithium still play an important economic role. From an economic perspective, decommissioned batteries will become the primary consideration of high-quality mines due to the shortage of resources. By the end of 202, China’s lithium reserves accounted for 6.31% of the world, of which more than 83% were salt lake lithium deposits, mainly distributed in poor natural environmental conditions such as the Qinghai-Tibet Plateau [11]. Because of the mining difficulties, lithium resources that are easy to exploit account for only about 1% of the world’s total [11]; thus, it is very dependent on overseas lithium imports. Besides, China also ranks first in cobalt consumption, with great external dependence. Furthermore, China is also short of nickel. With these considerations, the imports of this energy have great value.

Since 2021, the price for recovering lithium has been increasing with the high volume of new energy vehicles. On the one hand, the high metal price aggravated battery companies; on the other hand, the high price increased the performance of power battery recovery elasticity [11]. Based on the expected release of upstream material capacity, the market price of lithium and iron, or nickel, will fall in the long and medium terms.

It can be predicted that in the future, the imports of lithium will still rise due to the relevance of downstream industries. In the consumption field, the demand for consumer electronics products is expanding, laying a solid foundation for the consumption of lithium batteries. In the power field, the development of new energy vehicles in China has provided a good opportunity for the power lithium battery industry. In the energy storage field, the rise of the energy Internet would significantly drive the demand for energy storage, which in turn could drive the development of energy storage lithium batteries.

5. Conclusion

Carbon neutrality is the huge driver of China’s economic growth and transformation in the future. At the same time, it is China’s commitment to the whole world and China’s value pursuit of building a community with a shared future for mankind. At present, China’s neutral development has come to the fourth stage, where it is approaching the goal of achieving carbon neutrality. Achieving carbon neutrality can be a major challenge to any country in the way of economic and social development, including China, even though it offers many benefits. With the development of technology, more and more new energy resources are available, which will gradually reduce the cost of its application. It is worth mentioning that China’s new energy technology ranks the top in the world, especially the photovoltaic power generation technology. Moreover, the energy storage ability in China makes a breakthrough in the short link between power generation and electricity consumption in the new energy era. Given the development stage of China, China has a great dependence on new energy development. Therefore, the imports of energy such as coal and lithium will still be important for China. Carbon neutrality is of long-term strategic significance for China. It is an inevitable choice for China to change its energy structure to achieve carbon neutrality so as to further boost the Chinese economy.

[1] Zheng, G. Q. (2010). Thinking on new situation and tasks of addressing climate change for China after Copenhagen climate change conference 2009. Advances in Climate Change Research, 6(2), 79-82.

[2] Mallapaty, S. (2020). How China could be carbon neutral by mid-century. Nature, 586(7830), 482-483.

[3] Zhang, S., & Chen, W. (2022). China’s energy transition pathway in a carbon-neutral vision. Engineering, 14, 64-76.

[4] Sun, H., & Chen, F. (2022). The impact of green finance on China’s regional energy consumption structure based on system GMM. Resources Policy, 76, 102588.

[5] Jiayu, B., Xingang, W., Chaoshan, X., Zhiyong, Y., Shoutao, T., & He, C. (2021, March). Development Status and Measures to Promote the Development of Renewable Energy in China. In 2021 3rd Asia Energy and Electrical Engineering Symposium (AEEES) (pp. 1102-1107). IEEE.

[6] Muradov, N. Z., & Veziroğlu, T. N. (2008). “Green” path from fossil-based to hydrogen economy: an overview of carbon-neutral technologies. International journal of hydrogen energy, 33(23), 6804-6839.

[7] Xie, W., Guo, W., Shao, W., Li, F., & Tang, Z. (2021). Environmental and health Co-benefits of coal regulation under the carbon neutral target: a case study in anhui province, China. Sustainability, 13(11), 6498.

[8] Zhang, S. C., Yang, X. Y., Xu, W., & Fu, Y. J. (2021). Contribution of nearly-zero energy buildings standards enforcement to achieve carbon neutral in urban area by 2060. Advances in Climate Change Research, 12(5), 734-743.

[9] Shi, H., Chai, J., Lu, Q., Zheng, J., & Wang, S. (2022). The impact of China’s low-carbon transition on economy, society and energy in 2030 based on CO2 emissions drivers. Energy, 239, 122336.

[10] SWS Research. (2023). Solar Power Supply (300274). 22-24.

[11] Chen, X. (2023). Huaan Security Report. 7-8.

References

[1]. Zheng, G. Q. (2010). Thinking on new situation and tasks of addressing climate change for China after Copenhagen climate change conference 2009. Advances in Climate Change Research, 6(2), 79-82.

[2]. Mallapaty, S. (2020). How China could be carbon neutral by mid-century. Nature, 586(7830), 482-483.

[3]. Zhang, S., & Chen, W. (2022). China’s energy transition pathway in a carbon-neutral vision. Engineering, 14, 64-76.

[4]. Sun, H., & Chen, F. (2022). The impact of green finance on China’s regional energy consumption structure based on system GMM. Resources Policy, 76, 102588.

[5]. Jiayu, B., Xingang, W., Chaoshan, X., Zhiyong, Y., Shoutao, T., & He, C. (2021, March). Development Status and Measures to Promote the Development of Renewable Energy in China. In 2021 3rd Asia Energy and Electrical Engineering Symposium (AEEES) (pp. 1102-1107). IEEE.

[6]. Muradov, N. Z., & Veziroğlu, T. N. (2008). “Green” path from fossil-based to hydrogen economy: an overview of carbon-neutral technologies. International journal of hydrogen energy, 33(23), 6804-6839.

[7]. Xie, W., Guo, W., Shao, W., Li, F., & Tang, Z. (2021). Environmental and health Co-benefits of coal regulation under the carbon neutral target: a case study in anhui province, China. Sustainability, 13(11), 6498.

[8]. Zhang, S. C., Yang, X. Y., Xu, W., & Fu, Y. J. (2021). Contribution of nearly-zero energy buildings standards enforcement to achieve carbon neutral in urban area by 2060. Advances in Climate Change Research, 12(5), 734-743.

[9]. Shi, H., Chai, J., Lu, Q., Zheng, J., & Wang, S. (2022). The impact of China’s low-carbon transition on economy, society and energy in 2030 based on CO2 emissions drivers. Energy, 239, 122336.

[10]. SWS Research. (2023). Solar Power Supply (300274). 22-24.

[11]. Chen, X. (2023). Huaan Security Report. 7-8.

Cite this article

Zheng,Y. (2023). The Impact of Carbon-neutral Planning on China's Economy. Advances in Economics, Management and Political Sciences,35,55-62.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Volume title: Proceedings of the 7th International Conference on Economic Management and Green Development

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Zheng, G. Q. (2010). Thinking on new situation and tasks of addressing climate change for China after Copenhagen climate change conference 2009. Advances in Climate Change Research, 6(2), 79-82.

[2]. Mallapaty, S. (2020). How China could be carbon neutral by mid-century. Nature, 586(7830), 482-483.

[3]. Zhang, S., & Chen, W. (2022). China’s energy transition pathway in a carbon-neutral vision. Engineering, 14, 64-76.

[4]. Sun, H., & Chen, F. (2022). The impact of green finance on China’s regional energy consumption structure based on system GMM. Resources Policy, 76, 102588.

[5]. Jiayu, B., Xingang, W., Chaoshan, X., Zhiyong, Y., Shoutao, T., & He, C. (2021, March). Development Status and Measures to Promote the Development of Renewable Energy in China. In 2021 3rd Asia Energy and Electrical Engineering Symposium (AEEES) (pp. 1102-1107). IEEE.

[6]. Muradov, N. Z., & Veziroğlu, T. N. (2008). “Green” path from fossil-based to hydrogen economy: an overview of carbon-neutral technologies. International journal of hydrogen energy, 33(23), 6804-6839.

[7]. Xie, W., Guo, W., Shao, W., Li, F., & Tang, Z. (2021). Environmental and health Co-benefits of coal regulation under the carbon neutral target: a case study in anhui province, China. Sustainability, 13(11), 6498.

[8]. Zhang, S. C., Yang, X. Y., Xu, W., & Fu, Y. J. (2021). Contribution of nearly-zero energy buildings standards enforcement to achieve carbon neutral in urban area by 2060. Advances in Climate Change Research, 12(5), 734-743.

[9]. Shi, H., Chai, J., Lu, Q., Zheng, J., & Wang, S. (2022). The impact of China’s low-carbon transition on economy, society and energy in 2030 based on CO2 emissions drivers. Energy, 239, 122336.

[10]. SWS Research. (2023). Solar Power Supply (300274). 22-24.

[11]. Chen, X. (2023). Huaan Security Report. 7-8.