1. Introduction

The photovoltaic industry covers aspects such as the manufacturing of solar cells and the design of photovoltaic systems. In recent years, the current situation of China's photovoltaic industry is attracting attention. According to forecasts, in 2024, China's photovoltaic market will reach 204.7GW, and the photovoltaic assembly capacity has reached the world in the world. First, photovoltaic power generation also follows the growth, and the proportion of new energy power generation capacity in the country will continue. The Chinese government has released a series of policies to support the development of the photovoltaic industry as the main energy sources of the country. To increase the photovoltaic industry to 1.3TW in 2030. In recent years, the U.S. government has adopted a series of policies and implementation measures to develop the photovoltaic industry, such as improving the investment environment of the photovoltaic industry, unique policy support in various states, and implementing high benefits, high subsidies and tax reduction policies in the photovoltaic industry, etc. The government makes many outstanding results in the world in terms of policy and continuous innovation, but in the process of development, there are some disadvantages:

i: China has gradually moved from centralized to distributed photovoltaics in the past. What problems are China facing in photovoltaic power generation now? What is the solution?

ii: In 2025, the first batch of photovoltaic solar panels in China will be retired. After retirement, where will these discarded batteries go? What is the solution?

iii: Is the United States using centralized or distributed industries? What are the geographical advantages of the distributed regions and what problem will they face? What is the attitude of the US government towards this industry?

iv: Both China and the United States face enormous challenges in the photovoltaic industry. Analyzing the relationship between the photovoltaic industries of China and the United States in terms of international status, the advantages and disadvantages of using distributed methods, and the advantages and disadvantages of solving these problems. What trends will the future lead to?

The above questions will use representative states or provinces to compare centralized and distributed photovoltaics in China and the United States, as well as to study and analyze the current situation and trends of the solar photovoltaic industry in China and the United States. Research can be found. The flexibility of policies and the economic support provided by the government are important aspects of developing the photovoltaic industry. Solar photovoltaics will dominate global energy consumption in the future. They are becoming the mainstay of the world while replacing traditional energy sources.

2. Industry Status

2.1. Current Situation of China's Industry

In the past decade of rapid development, the entire industry chain of China's photovoltaic industry has fully achieved independent intellectual property rights, which is one of the important driving forces for China to achieve an energy revolution in the future [1]. Photovoltaic power generation can be divided into centralized and distributed photovoltaics. Centralized photovoltaics refers to the construction of large-scale power generation measures on a large regional scale, with the characteristics of large-scale, efficient, and geographically concentrated power generation. Distributed photovoltaics is a new energy technology today. It utilizes dispersed resources in or near the user's location, such as roofs and floors, to build a photovoltaic power generation system, which belongs to small-scale power plants. However, centralized photovoltaics have a large investment and occupy a large area, most of which are distributed in the sunny and energy-rich northwest region of China, especially in the Yangtze River Delta and Pearl River Delta regions where there is a high electricity demand. These cross-regional power transmission processes cause significant losses and unstable photovoltaic power supply, and distributed photovoltaics solve these problems. They adapt to local conditions, are clean, and efficient, and fully utilize local solar energy resources, solve the problem of electricity shortage in local areas such as the Yangtze River Delta and Pearl River Delta, and achieve the common development of power generation and consumption.

At present, China is gradually shifting from centralized to distributed photovoltaics, but it has also brought a series of hidden dangers. The development of distributed photovoltaics is inconsistent with the planning process of the power grid and centralized power stations, and the actual conditions are affected. The power grid has not yet absorbed the electricity from centralized photovoltaic power stations, and now distributed photovoltaics are developing rapidly. This is a huge challenge for the power grid to absorb centralized electricity. In addition, distributed photovoltaics will change the original power grid and energy storage, no longer focusing on whether mandatory matching ratios are needed. Instead, it is necessary to conduct overall planning and analyze which areas can strengthen active distribution networks and configure energy storage. In recent years, extreme natural disasters have caused power outages or accidents in local areas for distributed photovoltaic power stations, and post-disaster maintenance and recovery of equipment are both important. A complex process poses a significant threat to the secure operation of distributed systems. But there is no doubt about it. Distributed photovoltaic power generation, due to its dispersed nature, is generally developed on idle roofs or factory roofs, which can effectively save increasingly scarce land resources. Based on subsidies and encouragement policies for distributed photovoltaic power generation in various regions, the standardized electricity cost of distributed photovoltaic power generation is significantly lower than the existing industrial and civil electricity prices, which will stimulate the enthusiasm of industrial and commercial factory owners to develop [2]. Therefore, stable and reliable electricity has become a top priority for most countries and cities.

Since 2003, China has issued a series of policies to encourage the development of the photovoltaic industry. These policies and their implementation have provided strong guidance in the face of problems such as power grid transmission or installation of power stations.

2.2. The Current State of the US Industry

There are two main types of policies in the US photovoltaic industry: management policies such as laws and regulations, standards, and binding indicators, and federal fiscal incentive plans. Representative policies include the 1603 Treasury Plan, Federal Accelerated Depreciation Cost Recovery System, Photovoltaic Investment Tax Reduction Policy, Solar Energy Tax Reduction Policy, etc [3]. Since 2009, the use of coal for power generation in the United States has continued to decline, gradually being replaced by renewable energy sources, such as hydrogen and solar energy. According to authoritative data, in 2022, the total scale power generation in public utilities in the United States reached 42400 kWh, and natural gas, as the main source of energy, accounted for 37% of natural gas in 2021 and increased by 4% in 2022. The share of renewable energy power generation also increased from 19% to 22%.

According to the IRA (Investment Reduction Act) bill and statewide proposals for renewable energy, the United States plans to achieve decarbonization of electricity by 2035 and carbon neutrality by 2050 as the ultimate goal. The main sources of electricity generation in the United States are natural gas, solar energy, and wind energy. Currently, the electricity consumption structure remains stable, and energy use is mainly industrial and commercial. Photovoltaic power plants in the United States are almost distributed in areas with abundant sunlight in the Southwest region, with California being the state with the largest installed solar photovoltaic power generation in China. In 2022, California's solar power generation capacity exceeded 3.7 billion tons, making it the state with the highest growth in solar capacity compared to Texas, which has flourished in recent years. Texas's main advantage lies in having a large amount of land, abundant sunlight, and climate, leading to rapid growth, Gradually, becoming a leader in the photovoltaic industry, but with the emergence of interconnection restrictions and other issues, relying solely on solar energy is not enough. Various industries need to innovate, and improving storage energy efficiency constantly is key, Moreover, a large number of photovoltaic modules in the United States are heavily dependent on imports, and the uncertainty of photovoltaic module supply and rising financing costs will further limit the installation speed of photovoltaics. In the long run, the challenge of achieving sustained growth in the photovoltaic industry is significant.

3. Development Trend of Photovoltaic Industry in China and the United States

3.1. China's Development Prospects

Although China forms a complete industrial chain in the photovoltaic industry, Having the resource conditions, technological advantages, and application foundation for the large-scale development of photovoltaic power generation systems, the energy consumption of each link in the industrial chain has steadily and rapidly decreased [4]. However, China's photovoltaic industry started relatively late, and there are still many shortcomings compared to mature and complete photovoltaic industries abroad, such as relatively high power generation costs and dependence on policy support, gaps in production technology and equipment compared to advanced foreign levels, and a lack of scientific planning for the photovoltaic industry. With the advancement of the dual carbon strategy goals and the 14th Five Year Plan, the global demand for the development of the photovoltaic industry will continue to increase, which is conducive to promoting capital inflows and photovoltaic technology innovation, thereby further promoting the development of the photovoltaic industry [5]. To solve the problems faced by photovoltaic power generation, corresponding measures need to be taken based on the existing problems. The following suggestions are proposed:

1) Utilizing the existing industrial layout and power system to guide distributed photovoltaics for photovoltaic assembly, planning more distributed photovoltaic installations in areas with concentrated power grids and greater tolerance for photovoltaic power generation uncertainty, and planning fewer installations in areas with weak power grids or mainly relying on external power input, can reduce land use area and achieve the most efficient utilization rate of photovoltaic installations.

2) So far, China's solar photovoltaics have gradually shifted from centralized to distributed. The photovoltaic power stations that were previously concentrated in the northwest region have now led to the problem of "light abandonment" because the first batch of photovoltaic panels in China will be "retired" in 2025, and there is currently no good way to recover some components for recycling. Therefore, while encouraging distributed photovoltaics, it needs to move forward steadily, Emphasizing the installation area of distributed installations and learning from the historical lessons of centralized photovoltaics has prevented a large number of underutilized components from being unable to be recycled after the retirement of solar photovoltaic panels for 20-30 years.

3) By combining industry types and constructing large-scale industrial parks as pilot projects for large and micro power grids, potential problems can be preliminarily and better explored. After accumulating experience in the pilot projects, development can be carried out simultaneously in multiple industrial parks. When assembling distributed photovoltaics in thousands of households in the future, the density of the power grid and the characteristics of electricity should be considered to promote them in a step-by-step manner, For remote rural areas, there is no need to urgently build a large number of large-scale photovoltaic power stations and government subsidies for promotion. The biggest challenge facing today is to promote the joint development of photovoltaic industry installation and power grid. As distributed photovoltaics reach millions of households, it also means that higher active distribution networks are needed, and higher requirements are needed for pairing detection systems.

4) In terms of climate, in the past, centralized photovoltaics were concentrated in the northwest region, facing only dry and high-temperature climate conditions, while distributed photovoltaics were mostly installed in developed areas in the east and south. In winter, the climate became humid, and the warm currents in the South Pacific led to an increase in rainfall. Especially in the south, distributed photovoltaics have become more frequent in responding to these small disasters and difficulties. Therefore, installing power in new areas means facing more complex climate change and electricity demand in various regions, which requires promoting the development of new smart grids that match it, including methods for predicting and supplying small disasters.

Only by being down-to-earth, adapting to market characteristics and needs, implementing policies in different regions, and adopting more flexible and diversified project cooperation strategies. At the same time, it needs to accelerate the localization of the industrial chain, avoid policy risks, promote local employment and technological improvement, and promote the deepening and implementation of international cooperation in photovoltaics [6].

3.2. Development Prospects of the United States

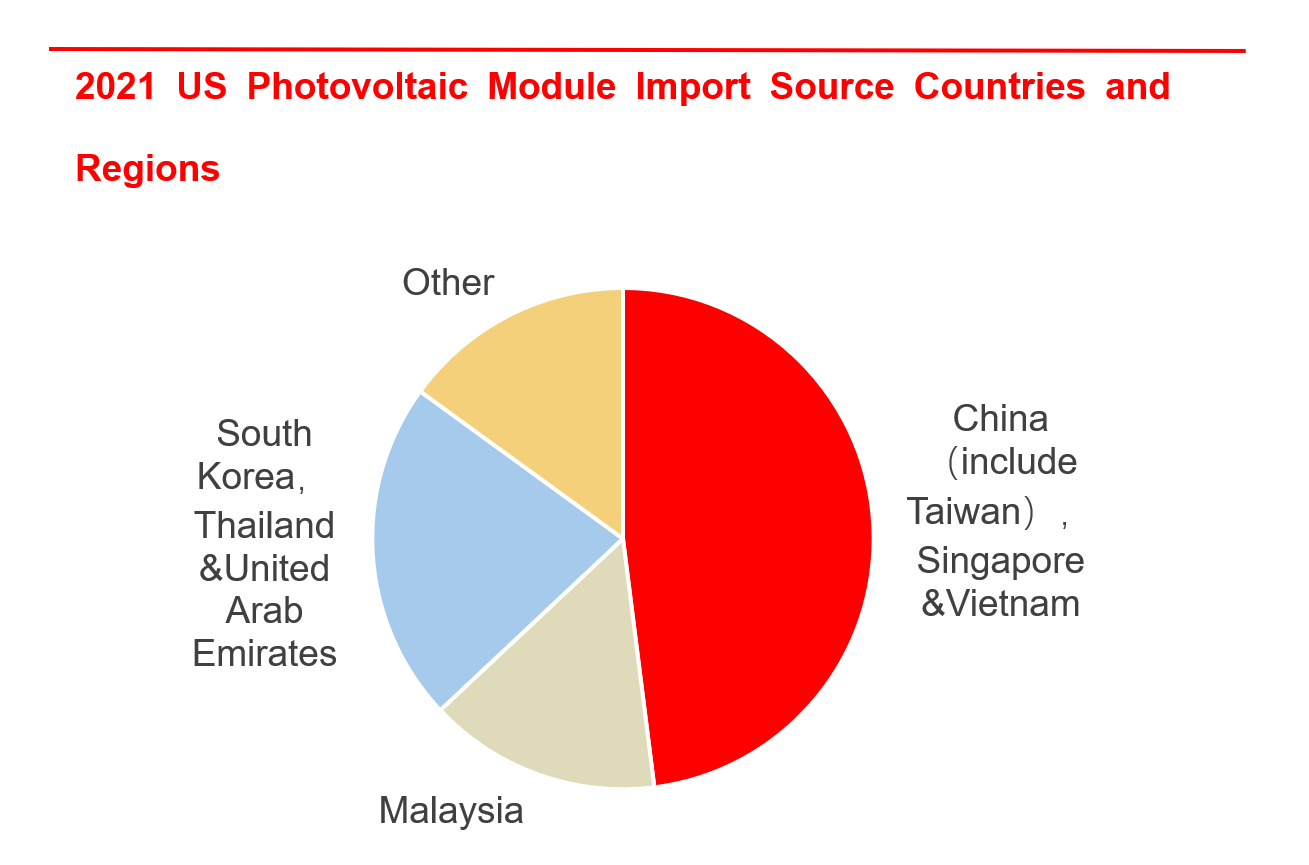

The development of the photovoltaic industry in the United States has a sound legal guarantee, and its industrial development policies are mainly manifested through federal energy legislation, federal environmental policy, state legislation, agricultural legislation, and other forms[3].In the past four years, the "double anti" (anti-dumping and anti-subsidy) policies implemented by the United States against China have actually led to an increase in the prices of photovoltaic products in the country, resulting in insufficient competitiveness compared to traditional energy. A large number of midstream and downstream enterprises have gone bankrupt, leading to a continuous decline in employment opportunities. Even though the United States has unique policy and geographical advantages in each state, and the planned growth of photovoltaic module production capacity is rapid, it cannot escape the influence of natural disasters, power grid and market reforms, and other practical factors. The United States relies on imported components, which increased from 2GW in 2010 to 13GW in 2016; The source countries of imports have gradually shifted to Asia since 2015, with two-thirds of imports coming from Malaysia, China, and South Korea in 2016. The price of photovoltaic modules has decreased by about 40% since 2012, with an average price of 1 $15 per watt, which decreased to $0.72 per watt in 2016, and had already dropped to $0 by the end of 2017 $45 per watt [3]. In May 2023, the US Environmental Protection Agency (EPA) proposed restrictions on greenhouse gas emissions from coal, oil, and other chemical fuel power plants. However, in August of the same year, four US grid operators commented to the EPA that they did not consider the reliability and sustainability of the power grid, resulting in a severe shortage of electricity in the United States. Fortunately, the United States has timely adjusted its strategy and carried out market-oriented reforms to ensure fair competition between the generation and sales sides of the electricity market, and fair access to transmission and distribution by independent system operators. So far, the IRA bill has provided certainty for subsidy policies for photovoltaic power generation in the United States, and the installed capacity of photovoltaic developers is gradually increasing. According to SEIA data, it is predicted that the current module production capacity in the United States will increase from less than 9GW to 90GW by 2025, At the same time, the component production capacity has exceeded 40GW, and there is hoped to reduce the import of components from the United States in 2023-2026, and achieve full utilization of domestic battery cells in 2027. However, from the perspective of component production forecasts, the demand is still greater than the supply, which also indicates that the United States will need to import some components in the future. The following are the sources of photovoltaic module imports from the United States in 2021, as shown in Figure 1.

Figure 1: 2021 US photovoltaic module import source countries and regions (Picture credit : Original)

4. Industry Comparison

The subsidies provided by the Chinese government have had a positive impact on the prosperity of the photovoltaic industry, cultivating numerous outstanding enterprises [7]. Although China lags behind the United States at the beginning of its photovoltaic industry, in recent years, China's photovoltaic industry has taken a leading position, with advantages such as its components and 90% of components being exported, resulting in considerable revenue from the photovoltaic industry. In February 2023, the "2022 Development Review and 2023 Situation Outlook Seminar of the Photovoltaic Industry" hosted by the China Photovoltaic Industry Association was successfully held. According to data, since 2022, multiple photovoltaic power generation policies have been introduced from the central to local governments in China, especially since the 14th Five Year Plan (the 14th Five Year Plan), photovoltaic power generation policies have reached a new level in the photovoltaic industry market in 2023, Centralized and distributed photovoltaic installations have achieved a significant increase. In 2021, the government issued some important notices, including three documents: "Completing the Signing and Performance of Medium - and Long-Term Electricity Contracts in 2022", "Accelerating the Progress of Electricity Spot Market Construction", and "Guiding Opinions on Building a National Electricity Unified Market System", to provide support for the participation of new energy in the photovoltaic electricity market. New energy is still on the growth trend globally, and new energy needs to adapt to the needs of the electricity market while also meeting the needs of the electricity market. It also need to plan the layout and provide hardware and software support.

At present, China has established a complete industrial chain from upstream silicon materials and equipment for photovoltaics, and midstream battery modules to downstream power generation systems, with an annual output value exceeding 500 billion yuan, accounting for more than 70% of the global annual output value [8]. The photovoltaic industry in the United States is mainly developed in a centralized manner. Although it is the birthplace of the photovoltaic industry and has many geographical advantages, the local new energy industry is at a development bottleneck in the manufacturing end, unable to utilize factories to produce a large number of components. Components rely on imports, and in terms of facilities, the photovoltaic industry has intermittent and unstable characteristics. The government has taken corresponding measures. For example, in terms of labor security, the government encourages traditional energy practitioners to switch to the renewable energy sector, deliver fresh blood to the photovoltaic manufacturing industry, build a complete industrial chain, and achieve comprehensive localization of the green manufacturing industry. In terms of trade policies, the government suspends trade control policies such as "double anti" and tariff protection and leverages the role of international partners to cope with major strategic competitors [8]. The photovoltaic industry chain in Southeast Asia is mainly invested and constructed by domestic manufacturers. Among them, Longi Group, Trina Solar, Jinko Energy, and Jingao Technology have established 13GW, 6GW, 7GW, and 4GW component factories in the four Southeast Asian countries, respectively. This policy demonstrates the shift in attitude of the United States towards China's new energy. However, China still faces many challenges when setting up factories in the United States. Whether it can pass the review of foreign investment in the United States, whether the project can proceed smoothly, whether it can be profitable in the actual operation process, and whether there will be many uncertainties in management, all of which require time to examine.

5. Conclusion

From this, it can be seen that both the governments of China and the United States have issued corresponding policies for the solar photovoltaic industry. This paper draw the following conclusion from this article: in addition to providing policy support, China and the United States have provided subsidies to enterprises, and have gained consensus in multiple aspects, The new energy market in the United States is a key overseas investment area that Chinese companies are focusing on. Chinese companies have also achieved good results in the US wind and solar markets. However, the problems faced by China's distributed and centralized systems in the United States also require timely measures to be taken. To reduce more losses in the future, this paper believed that China and the United States can cooperate, reach agreements in terms of funding and talent, continuously innovate in technology, and achieve a win-win situation.

References

[1]. Li, J.Q. (2021) Chasing Light Technology Yang Xi (in China): Seizing the Lead in the Organic Semiconductor Photovoltaic Track. Technology and Finance, 3, 51-54.

[2]. Li, M.D. Li, J.W. (2023) The Development Status and Prospects of Distributed Photovoltaic Power Generation in China under the "Dual Carbon" Goal. Solar Energy, 5, 5-10.

[3]. Yuan, J.Z. Wang, J. (2019) Comparative Analysis and Inspiration of Competitiveness in the Photovoltaic Industry between China and the United States. China Economic and Trade Journal, 7, 21-24.

[4]. Xiao, J. Mei, Q. Huang, X.Q. Jiang, L. Zhang, J.P. (2022) Current Status and Development Trends of Photovoltaic Power Generation Technology in China under the "Dual Carbon" Goal. Natural Gas Technology and Economy, 5, 64-69.

[5]. Zhu, Q.B. (2022) Review and Outlook on the Development of China's Photovoltaic Industry under the Vision of Carbon Neutrality. Jiangsu Business Review, 12, 91-93.

[6]. Chen, C.X. (2023) Research on the Current Situation and Trends of International Cooperation in China's Photovoltaic Industry. Sino Foreign Energy, 2, 21-26.

[7]. Huang, B. Zhao, W. Liao, L.D. Huang, J.L. Xie, P.L. Regional Differences Analysis of the Photovoltaic Industry Chain from a Policy Perspective. Southern Energy Construction, 1-10.

[8]. Zhao, S.S. Hua, M. Xiao, Q.Q. (2022) Global Photovoltaic Industry Development and Comparison between China and the United States. Zhangjiang Science and Technology Review, 4, 28-31.

Cite this article

Xie,Y. (2024). The Current Status and Development Trend of China and the United States Solar Photovoltaic Industry. Advances in Economics, Management and Political Sciences,83,271-277.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Volume title: Proceedings of the 2nd International Conference on Management Research and Economic Development

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Li, J.Q. (2021) Chasing Light Technology Yang Xi (in China): Seizing the Lead in the Organic Semiconductor Photovoltaic Track. Technology and Finance, 3, 51-54.

[2]. Li, M.D. Li, J.W. (2023) The Development Status and Prospects of Distributed Photovoltaic Power Generation in China under the "Dual Carbon" Goal. Solar Energy, 5, 5-10.

[3]. Yuan, J.Z. Wang, J. (2019) Comparative Analysis and Inspiration of Competitiveness in the Photovoltaic Industry between China and the United States. China Economic and Trade Journal, 7, 21-24.

[4]. Xiao, J. Mei, Q. Huang, X.Q. Jiang, L. Zhang, J.P. (2022) Current Status and Development Trends of Photovoltaic Power Generation Technology in China under the "Dual Carbon" Goal. Natural Gas Technology and Economy, 5, 64-69.

[5]. Zhu, Q.B. (2022) Review and Outlook on the Development of China's Photovoltaic Industry under the Vision of Carbon Neutrality. Jiangsu Business Review, 12, 91-93.

[6]. Chen, C.X. (2023) Research on the Current Situation and Trends of International Cooperation in China's Photovoltaic Industry. Sino Foreign Energy, 2, 21-26.

[7]. Huang, B. Zhao, W. Liao, L.D. Huang, J.L. Xie, P.L. Regional Differences Analysis of the Photovoltaic Industry Chain from a Policy Perspective. Southern Energy Construction, 1-10.

[8]. Zhao, S.S. Hua, M. Xiao, Q.Q. (2022) Global Photovoltaic Industry Development and Comparison between China and the United States. Zhangjiang Science and Technology Review, 4, 28-31.