1. Introduction

Mounting societal demands for dual economic-environmental performance exert unprecedented operational pressures on corporations. Given finite allocatable resources, firms frequently resort to symbolic environmentalism ("greenwashing") [1]—minimizing ecological investments while projecting pro-environmental images. This decoupling practice yields suboptimal environmental outcomes and impedes China's sustainable transition toward high-quality development.

Scholarly consensus categorizes greenwashing determinants into three dimensions, Corporate financial traits: Tightened capital constraints trigger greenwashing [2]; independent verification curbs such behaviors [3]; rising marketing expenditures increase greenwashing risks [4]; poor ESG performance heightens susceptibility [5]. Macro-regulatory factors: Environmental monitoring decentralization suppresses greenwashing [6]; green credit policies initially exacerbate but ultimately mitigate greenwashing through eco-innovation incentives [7]. Market-Industry drivers: Environmentally sensitive sectors exhibit significantly lower greenwashing incidence [8]. Collectively, extant literature identifies three anti-greenwashing pathways: alleviating financial constraints, fostering authentic green initiatives, and strengthening regulatory oversight.

Departing from prior studies, this research examines China's 2018 VAT credit refund policy as a novel greenwashing deterrent. Using 2012-2022 panel data from non-financial A-share listed firms, we employ a quasi-experimental DID design to quantify its impact on corporate environmental misrepresentation.

2. Theoretical analysis and hypothesis research

2.1. Policy-greenwashing nexus

The VAT carryforward refund policy potentially influences corporate environmental strategies through two theoretically distinct yet interrelated transmission channels. The capital liquidity channel operates through direct fiscal transfers: By refunding accumulated input VAT credits, the policy immediately enhances corporate cash positions via tangible resource effects while simultaneously signaling regulatory benevolence—reducing precautionary cash hoarding behaviors [9]. This dual mechanism effectively lowers capital acquisition costs and alleviates binding financing constraints [10], consequently diminishing firms' rational incentives to engage in resource-conserving environmental misrepresentation [11].

Simultaneously, the innovation incentive channel functions as a targeted fiscal subsidy: By reducing the effective marginal cost of research and development (R&D) expenditures, the policy reorients capital allocation toward technological innovation [12]. This structural shift accelerates development and adoption of authentic green production technologies, thereby elevating substantive environmental performance benchmarks. As firms' genuine ecological capabilities strengthen, the utilitarian rationale for maintaining symbolic environmental facades progressively erodes.

Integrating these theoretical propositions, we formally hypothesize:

H1: Implementation of the VAT carryforward refund policy generates statistically significant suppression effects on corporate greenwashing behaviors.

2.2. Value-added tax carry-forward refund policy, green innovation, corporate "greenwashing" behavior

Regarding mediating mechanisms, the policy's conversion of illiquid tax credits into fungible capital reserves fundamentally transforms corporate financial flexibility. Post-implementation, enterprises gain substantial autonomy in deploying these fiscal resources, with observable innovation-enhancing effects materializing through two complementary pathways. First, green factor augmentation manifests through increased investments in human capital (notably high-skilled technicians via capital-skill complementarity [13]), expanded R&D budgets (owing to reduced innovation costs [14]), and dedicated environmental asset acquisitions [15]. Second, liquidity constraint relaxation reduces precautionary cash reserves per Keynesian monetary theory, bolstering investor confidence and redirecting capital toward innovation projects with demonstrable stock return premiums [16]. Consequently, we advance:

H2: The policy's greenwashing-suppressing effects operate primarily through enhanced green innovation capacities.

3. Research design

3.1. Sample selection and data sources

Our sample comprises Chinese A-share non-financial firms observed from 2012 to 2022. Greenwashing metrics were sourced from Bloomberg/Wind ESG databases, financial variables from the CSMAR database, and eco-innovation indicators from the CNRDS database. To ensure data integrity, we excluded financially distressed firms (ST/*ST/PT status) during the sample period and applied 1% Winsorization to continuous variables, retaining 7,350 firm-year observations.

3.2. Variable definition

3.2.1. The dependent variable

Corporate greenwashing intensity quantified as the standardized within-industry divergence between externally reported ESG disclosure scores and independently verified environmental performance metrics [2].

3.2.2. Core explanatory variable

The quasi-natural experiment design necessitates precise identification of treatment exposure: Temporal dimension (Post): Binary indicator coded 1 for the policy implementation period (2018–2022) and 0 for the pre-intervention phase (2012–2017). Enterprise eligibility (Treat): Dummy variable assigned 1 if the firm's primary industry classification aligns with the Ministry of Finance's Catalog for VAT Credit Refund Policy Eligibility, and 0 otherwise.The interaction term Post×Treat constitutes our key regressor, capturing the causal effect of policy exposure on greenwashing behaviors within the difference-in-differences framework.

3.2.3. Mediating variable

The VAT mortgage refund policy in our country can promote green innovation in enterprises [13]. Green innovation can restrain the motivation of enterprises to engage in "greenwashing" [17]. Therefore, this paper selects green innovation as the mediating variable through which this policy can inhibit enterprises' "greenwashing" behavior. This paper measures green innovation by taking the natural logarithm of the sum of the number of independent green inventions and green utility models applied by enterprises in the same year, plus one.

3.2.4. Control variable

Drawing on prior research [13], this study employs fundamental financial metrics including firm size (Size), leverage ratio (Lev), and return on assets (Roa), along with firm-level controls such as board size (Board), company age (FirmAge), ownership concentration of the top ten shareholders (Top10), Big Four auditor engagement (Big4), and CEO duality (Dual).

3.3. Model construction

In order to study the impact of China's VAT carry-forward refund policy on the "greenwashing" behavior of listed companies, this paper takes the promulgation of the VAT carry-forward refund policy in 2018 as a quasi-natural experiment and constructs a difference-in-differences model:

To study the mechanism of the impact of the VAT carry-forward tax refund policy on the "greenwashing" behavior of enterprises, this paper establishes the following mediating effect model:

4. Empirical results and analysis

4.1. Baseline regression

Table 1 presents progressively specified regression outcomes. Column (1) controls only for firm and year fixed effects, revealing a statistically significant policy effect of -0.170 (t = -3.96). Column (2) incorporates financial and governance controls absent fixed effects, strengthening the estimated coefficient to -0.287 (t = -11.22). The comprehensive specification in Column (3) integrates both control variables and fixed effects, yielding a precisely estimated coefficient of -0.156 (t = -3.65) significant at the 1% level. This indicates that policy-eligible enterprises reduced greenwashing intensity by approximately 15.6 percentage points relative to control firms, providing robust confirmation of H1. Control variables exhibit economically intuitive signs: Larger firms (Size) demonstrate reduced greenwashing, while profitability (Roa) correlates positively with environmental transparency.

|

Variable |

(1) |

(2) |

(3) |

|

GWS |

GWS |

GWS |

|

|

Treat×Post |

-0.170*** |

-0.287*** |

-0.156*** |

|

(-3.96) |

(-11.22) |

(-3.65) |

|

|

Size |

-0.103*** |

-0.129*** |

|

|

(-8.89) |

(-3.53) |

||

|

Lev |

-0.063 |

0.290 |

|

|

(-0.81) |

(1.86) |

||

|

Roa |

0.455* |

0.990*** |

|

|

(2.16) |

(3.97) |

||

|

Board |

-0.069 |

0.215 |

|

|

(-1.11) |

(1.40) |

||

|

FirmAge |

0.204*** |

-0.369 |

|

|

(4.87) |

(-1.45) |

||

|

Top10 |

0.878 |

0.551** |

|

|

(10.52) |

(2.96) |

||

|

Balance |

0.210 |

0.064 |

|

|

(10.64) |

(1.40) |

||

|

Big4 |

0.594 |

0.396*** |

|

|

(14.91) |

(3.71) |

||

|

Dual |

0.214 |

0.034 |

|

|

(7.01) |

(0.81) |

||

|

Enterprise fixed effect |

Controled |

Uncontrolled |

Controled |

|

Fixed effect of time |

Controled |

Uncontrolled |

Controled |

|

Observation value |

7221 |

7340 |

7211 |

|

Adjusted R2 |

0.463 |

0.088 |

0.466 |

4.2. Testing of the intermediary mechanism

|

Variable |

(1) |

(2) |

|

GI |

GWS |

|

|

Treat×Post |

0.092*** |

-0.149*** |

|

(3.56) |

(-3.48) |

|

|

Green Innovation |

-0.080*** |

|

|

(-3.64) |

||

|

Control variables |

Yes |

Yes |

|

Fixed effect |

Controled |

Controled |

|

Observation value |

7211 |

7211 |

|

Adjusted R2 |

0.705 |

0.468 |

Table 2 delineates the transmission mechanism. Column (1) establishes that the policy significantly enhances green innovation outputs (β = 0.092, t = 3.56). Column (2) demonstrates that introducing green innovation (GI) into the greenwashing equation yields a significantly negative coefficient (γ₁ = -0.080, t = -3.64), while the direct policy effect (γ₂ = -0.149, t = -3.48) persists. This pattern confirms partial mediation—approximately 51.3% of the total policy effect operates indirectly through innovation channels—thereby validating H2.

4.3. Robustness test

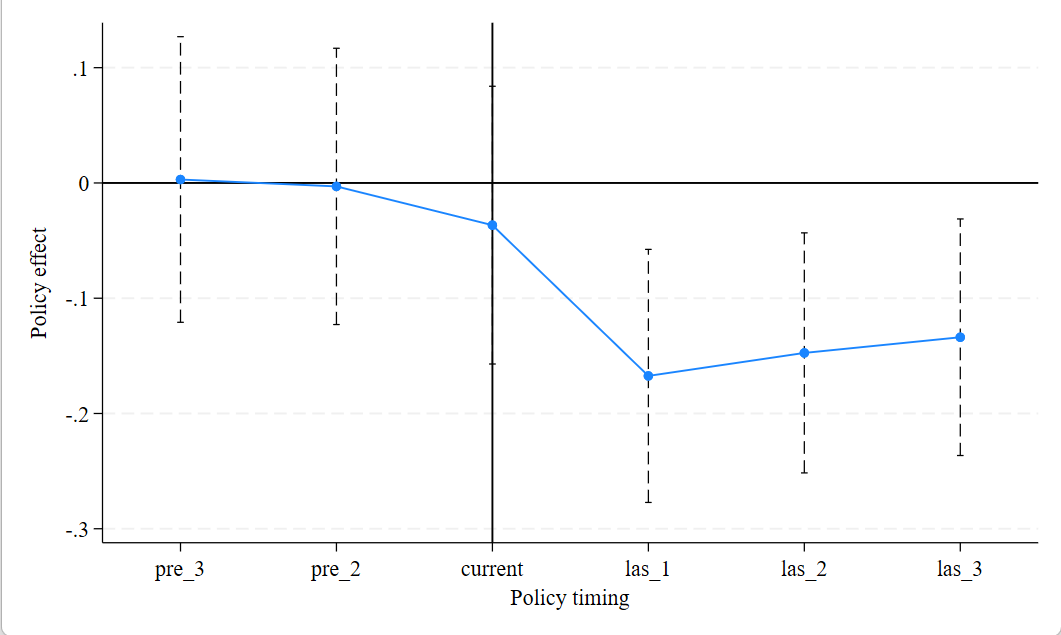

4.3.1. Parallel trend test

In order to demonstrate the reliability and rationality of the model selection in this paper, a parallel trend test is conducted here. Taking 2017 as the base year, it is examined whether the parallel trend assumption is met for the control group and the treatment group before the implementation of the policy, and whether the differences in variables between the two groups are significant after the policy is implemented. The model is established as follows:

Among them,

The results show that the policy estimated coefficient

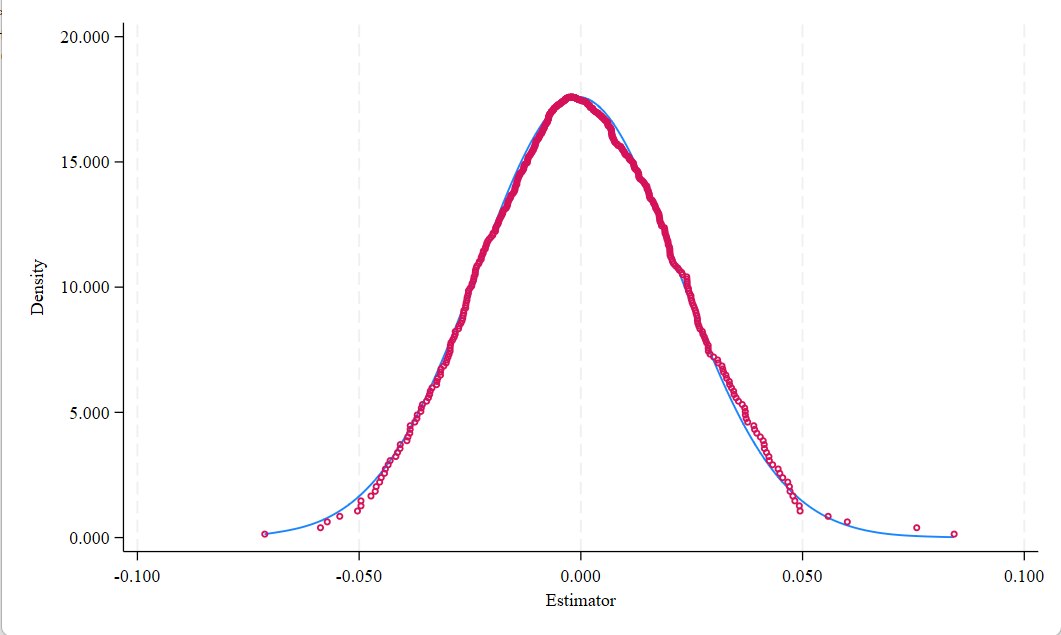

4.3.2. Placebo test

In order to avoid the significant influence of accidental correlations and policy choice biases on the robustness of the research results, this paper conducts 500 random sampling simulations on the sample. Figure 2 shows that the random estimated coefficients of

4.3.3. Add model control variables

In order to avoid missing the influence of key explanatory variables on the model's robustness and to further improve the model's prediction accuracy, this paper adds the management shareholding ratio at the company level (Mshare), the Herfindahl index at the industry level (HHI), and the environmental regulatory intensity at the regional level (Regulation) as supplementary control variables. The regression results are shown in Table 3. (1) to (3) columns add each of the three control variables one by one. The regression results show that after adding the control variables, the regression coefficients of the core explanatory variables remain significantly negative at the 1% level, and the research conclusion is consistent with the previous text, indicating that the results are robust.

|

Variable |

(1) |

(2) |

(3) |

|

GWS |

GWS |

GWS |

|

|

Treat×Post |

-0.151*** |

-0.161*** |

-0.154*** |

|

(-3.41) |

(-3.63) |

(-3.60) |

|

|

Control variables |

Yes |

Yes |

Yes |

|

Fixed effect |

Controled |

Controled |

Controled |

|

Observation value |

7221 |

7340 |

7211 |

|

Adjusted R2 |

0.552 |

0.552 |

0.552 |

4.4. Heterogeneity test

In order to further explore the mechanism by which the VAT carry-forward refund policy affects enterprises' "greenwashing" behavior, this paper examines the different impacts of this policy on enterprises with different characteristics from the perspectives of enterprise ownership, regional distribution, and capital intensity. The results are shown in Table 5.

|

Variable |

GWS |

||||||

|

State-owned enterprises |

Non-state-owned enterprises |

Businesses in the Midwestern region |

Enterprises in the eastern region |

High capital intensity |

Low capital intensity |

||

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

||

|

Treat×Post |

-0.213*** |

-0.048 |

-0.270*** |

-0.108* |

-0.170* |

-0.040 |

|

|

(-3.82) |

(-0.69) |

(-3.60) |

(-2.09) |

(-2.44) |

(-0.63) |

||

|

Control variables |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

|

Fixed effect |

Controled |

Controled |

Controled |

Controled |

Controled |

Controled |

|

|

Observation value |

4033 |

3178 |

2298 |

4913 |

3144 |

3933 |

|

|

Adjusted R2 |

0.466 |

0.465 |

0.431 |

0.484 |

0.474 |

0.491 |

|

Columns (1) and (2) of Table 5 show that the "greenwashing" behavior of enterprises of different ownerships is differently affected by the VAT carry-forward refund policy. According to the comparison of the estimated coefficients of the core explanatory variables, the policy has a stronger inhibitory effect on the "greenwashing" behavior of state-owned enterprises than that of non-state-owned enterprises. Columns (3) and (4) of Table 5 show that the "greenwashing" behavior of enterprises in different regions is differently affected by the VAT carry-forward refund policy. The results show that enterprises in the central and western regions are significantly more affected than those in the eastern region. Columns (5) and (6) of Table 5 show that the "greenwashing" behavior of enterprises with different capital intensities is differently affected by the VAT carry-forward refund policy. The results show that the inhibitory effect of the policy on the "greenwashing" behavior of high capital intensity enterprises is significantly stronger than that of low capital intensity enterprises.

5. Research conclusions and policy recommendations

5.1. Research conclusion

This investigation establishes robust causal evidence that China's VAT credit refund policy significantly attenuates corporate environmental misrepresentation, primarily through stimulating authentic green innovation. The average treatment effect of approximately 15.6% reduction in greenwashing intensity withstands rigorous identification checks, including parallel trend validation, placebo counterfactuals, and extensive model specifications. Crucially, we document substantial effect heterogeneity—revealing amplified efficacy among state-owned enterprises, firms in less developed regions, and capital-intensive industries. These findings collectively advance our understanding of fiscal instruments' capacity to realign corporate environmental strategies.

5.2. Policy recommendations

Building upon these empirical insights, we propose three targeted policy enhancements: Innovation-Linked Refund Premiums: Establish explicit fiscal incentives directing refunded capital toward green R&D—such as tiered refund multipliers for verifiable environmental technology investments—to strengthen the established innovation transmission channel. Ownership-Tailored Implementation: Calibrate refund magnitudes to address observed heterogeneity, particularly augmenting reimbursement rates for non-SOEs to overcome their attenuated responsiveness and amplify market-wide impacts. Regional Policy Integration: Strategically embed VAT refund mechanisms within existing ecological modernization initiatives—exemplified by designating "Green Innovation Reform Experimental Zones" where enterprises receive elevated refund ratios conditional on environmental performance benchmarks.

References

[1]. Huang Songbing, Xie Xiaojun, Zhou Huifen. The "Isomorphic" Behavior of Corporate Greenwashing [J]. China Population, Resources and Environment, 2020, 30(11): 139-150.

[2]. Zhang D. Green financial system regulation shock and greenwashing behaviors: Evidence from Chinese firms [J]. Energy Economics, 2022, 111: 106064.

[3]. Huang Songbing, Chu Fang. Does Third-Party Verification Help to Suppress Corporate "Greenwashing"? [J]. Chinese Certified Public Accountants, 2021, (08): 38-42. DOI: 10.16292/j.cnki.issn1009-6345.2021.08.009.

[4]. Cao J, Faff R, He J, et al. Who's greenwashing via the media and what are the consequences? Evidence from China [J]. Abacus, 2022, 58(4): 759-786.

[5]. Lee M T, Raschke R L. Stakeholder legitimacy in firm greening and financial performance: What about greenwashing temptations? ☆ [J]. Journal of Business Research, 2023, 155: 113393.

[6]. Zhang D. Can environmental monitoring power transition curb corporate greenwashing behavior? [J]. Journal of Economic Behavior & Organization, 2023, 212: 199-218.

[7]. He L, Gan S, Zhong T. The impact of green credit policy on firms’ green strategy choices: green innovation or green-washing? [J]. Environmental Science and Pollution Research, 2022, 29(48): 73307-73325.

[8]. Ruiz-Blanco S, Romero S, Fernandez-Feijoo B. Green, blue or black, but washing–What company characteristics determine greenwashing? [J]. Environment, Development and Sustainability, 2022, 24(3): 4024-4045.

[9]. Xie Y, Qin J, Jin Z, et al. VAT Neutrality and Corporate Cash Holdings—Based on the Research of Uncredited VAT Refund Policy [J]. China Finance and Economic Review, 2023, 12(2): 49-71.

[10]. Yue Shumin, Xiao Chunming. Can VAT carry-forward tax refunds alleviate enterprises' financing constraints? - Empirical evidence based on cash-cash flow sensitivity [J]. Finance and Trade Economics, 2023, 44(01): 51-67. DOI: 10.19795/j.cnki.cn11-1166/f.2023.01.003.

[11]. Zhang D. Are firms motivated to greenwash by financial constraints? Evidence from global firms' data [J]. Journal of international financial management & accounting, 2022, 33(3): 459-479.

[12]. Wang H, Yang J, Zhu N. Does Tax Incentives Matter to Enterprises’ Green Technology Innovation? The Mediating Role on R&D Investment [J]. Sustainability, 2024, 16(14): 5902.

[13]. Zhang Ming, Jiang Ou Chen, Cai Zhiqiang. Value-added Tax Carryforward Tax Rebate Policy and Enterprise Green Innovation [J]. Accounting and Finance Monthly, 2025, 46(08): 52-61. DOI: 10.19641/j.cnki.42-1290/f.2025.08.008.

[14]. Cai Weixian, Shen Xiaoyuan, Li Bingcai, et al. The Innovative Incentive Effect of VAT Carryforward Tax Rebate Policy [J]. Finance Research, 2022, (05): 31-48. DOI: 10.19477/j.cnki.11-1077/f.2022.05.005.

[15]. Li Yifei. VAT Carryforward Tax Rebate and Enterprise Human Capital Upgrading [J]. World Economy, 2023, 46(12): 115-140. DOI: 10.19985/j.cnki.cassjwe.2023.12.007.

[16]. Liu Bai, Wang Xinzhu. The "Risk Compensation" Effect of Enterprise Green Innovation on Stock Returns [J]. Economic Management, 2021, 43(07): 136-157. DOI: 10.19616/j.cnki.bmj.2021.07.009.

[17]. Ma Y, Feng G F, Yin Z, et al. ESG disclosures, green innovation, and greenwashing: All for sustainable development? [J]. Sustainable Development, 2025, 33(2): 1797-1815.

Cite this article

Yan,Z. (2025). Research on the Impact of VAT Carryover Refund Policy on Corporate "Greenwashing" Behavior. Advances in Economics, Management and Political Sciences,206,66-75.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Volume title: Proceedings of ICEMGD 2025 Symposium: Digital Transformation in Global Human Resource Management

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Huang Songbing, Xie Xiaojun, Zhou Huifen. The "Isomorphic" Behavior of Corporate Greenwashing [J]. China Population, Resources and Environment, 2020, 30(11): 139-150.

[2]. Zhang D. Green financial system regulation shock and greenwashing behaviors: Evidence from Chinese firms [J]. Energy Economics, 2022, 111: 106064.

[3]. Huang Songbing, Chu Fang. Does Third-Party Verification Help to Suppress Corporate "Greenwashing"? [J]. Chinese Certified Public Accountants, 2021, (08): 38-42. DOI: 10.16292/j.cnki.issn1009-6345.2021.08.009.

[4]. Cao J, Faff R, He J, et al. Who's greenwashing via the media and what are the consequences? Evidence from China [J]. Abacus, 2022, 58(4): 759-786.

[5]. Lee M T, Raschke R L. Stakeholder legitimacy in firm greening and financial performance: What about greenwashing temptations? ☆ [J]. Journal of Business Research, 2023, 155: 113393.

[6]. Zhang D. Can environmental monitoring power transition curb corporate greenwashing behavior? [J]. Journal of Economic Behavior & Organization, 2023, 212: 199-218.

[7]. He L, Gan S, Zhong T. The impact of green credit policy on firms’ green strategy choices: green innovation or green-washing? [J]. Environmental Science and Pollution Research, 2022, 29(48): 73307-73325.

[8]. Ruiz-Blanco S, Romero S, Fernandez-Feijoo B. Green, blue or black, but washing–What company characteristics determine greenwashing? [J]. Environment, Development and Sustainability, 2022, 24(3): 4024-4045.

[9]. Xie Y, Qin J, Jin Z, et al. VAT Neutrality and Corporate Cash Holdings—Based on the Research of Uncredited VAT Refund Policy [J]. China Finance and Economic Review, 2023, 12(2): 49-71.

[10]. Yue Shumin, Xiao Chunming. Can VAT carry-forward tax refunds alleviate enterprises' financing constraints? - Empirical evidence based on cash-cash flow sensitivity [J]. Finance and Trade Economics, 2023, 44(01): 51-67. DOI: 10.19795/j.cnki.cn11-1166/f.2023.01.003.

[11]. Zhang D. Are firms motivated to greenwash by financial constraints? Evidence from global firms' data [J]. Journal of international financial management & accounting, 2022, 33(3): 459-479.

[12]. Wang H, Yang J, Zhu N. Does Tax Incentives Matter to Enterprises’ Green Technology Innovation? The Mediating Role on R&D Investment [J]. Sustainability, 2024, 16(14): 5902.

[13]. Zhang Ming, Jiang Ou Chen, Cai Zhiqiang. Value-added Tax Carryforward Tax Rebate Policy and Enterprise Green Innovation [J]. Accounting and Finance Monthly, 2025, 46(08): 52-61. DOI: 10.19641/j.cnki.42-1290/f.2025.08.008.

[14]. Cai Weixian, Shen Xiaoyuan, Li Bingcai, et al. The Innovative Incentive Effect of VAT Carryforward Tax Rebate Policy [J]. Finance Research, 2022, (05): 31-48. DOI: 10.19477/j.cnki.11-1077/f.2022.05.005.

[15]. Li Yifei. VAT Carryforward Tax Rebate and Enterprise Human Capital Upgrading [J]. World Economy, 2023, 46(12): 115-140. DOI: 10.19985/j.cnki.cassjwe.2023.12.007.

[16]. Liu Bai, Wang Xinzhu. The "Risk Compensation" Effect of Enterprise Green Innovation on Stock Returns [J]. Economic Management, 2021, 43(07): 136-157. DOI: 10.19616/j.cnki.bmj.2021.07.009.

[17]. Ma Y, Feng G F, Yin Z, et al. ESG disclosures, green innovation, and greenwashing: All for sustainable development? [J]. Sustainable Development, 2025, 33(2): 1797-1815.