1. Introduction

The color green has become the color of our era. There is a broad agreement that environmental sustainability is vital for politics, the economy and culture to ensure the future of humanity [1]. As a vital part of economic society, enterprises play an undeniable role in environmental protection and pollution control [2].

In economic terms, green finance is a key means of achieving a low-carbon and climate-resilient economy [3], playing a significant role in promoting the harmonious coexistence of the economy and the environment [4]. Some scholars have expressed concerns over the environmental benefits of green bonds [5], suggesting that companies may be using them to enhance their "green, sustainable" image [6].

The term 'greenwashing' was first used in the 1960s, when the hotel industry came up with one of the most obvious examples of greenwashing. The environment could be saved if guests were asked to reuse their towels – the hotel put up notices in the rooms for this very reason. The hotels enjoyed the benefit of lower laundry costs. At present, the issue pertains to specious assertions, ambiguous phrasing, and the judicious selection of data, all of which collectively serve to engender a specious impression of environmental responsibility [7]. But it is a lack of a standard definition, due to its multifaceted nature, there isn't a single, universally accepted definition of greenwashing, leading to some ambiguity in its application.

Nowadays, based on institutional theory, stakeholder theory and signaling theory, researchers have explored the background and mechanism of “greenwashing” behavior. The research area has expanded from environmental behavior and social responsibility to ESG (environmental, social and governance) and supply chain management. In addition, the research on the form of “greenwashing” has expanded from environmental information disclosure and value proposition to visual image and sustainable strategy [8].

Meanwhile, most studies adopt conceptual speculation and observation methods, lacking empirical tests on the macro consequences of "greenwashing" behaviors and the effectiveness of governance measures. Secondly, the sample scope is limited, which is also a research gap. The research samples are mostly concentrated on listed companies that disclose annual reports and social responsibility reports, lacking investigations of general enterprises. Moreover, since "greenwashing" is a complex and multidimensional phenomenon, it is difficult to collect accurate data and obtain objective "greenwashing" measurement values, resulting in relatively few empirical studies.

This paper mainly discusses the impact of greenwashing in the company, and explores the impact of green washing on a company's stock financial performance? For this question, there are two hypotheses, one is H0: Green washing would harm the financial performance of companies, and the other is H1: Greenwashing would improve the financial performance of companies. To research it, event study is a good choice. This method can reveal the market's reaction to an event by comparing stock price movements before and after the event. This paper analyses the data by setting the Event Window [-10, +10], distinguishing the market performance before and after the event. This research provides a foundation for future studies on greenwashing. Meanwhile, through the comparison of stock prices, it enables the public to have a better understanding of the impact of greenwashing on companies. It also serves as a warning for potential greenwashing in the future and calls for people to increase their knowledge about greenwashing and ESG.

2. Literature review

Tackling environmental issues can boost a company's eco-friendly reputation and give it a major edge over the competition [9]. Legitimacy and reputation among various stakeholders can be improved by communicating eco-friendly activities through green disclosure [10]. Nevertheless, the issue of whether the release of green bonds truly prompts businesses to make eco-friendly investments or if companies instead engage in greenwashing, falsifying the scope of their green investments, is a significant worry for both scholars and practitioners. Traditionally, the term "greenwashing" has been used to refer to the practice whereby false or exaggerated claims are made by companies about their environmental responsibilities, with selective disclosure of information or presentation of misleading narratives being used [11].

Although there is still no easy answer to stop greenwashing, there are different ways that politicians and the law can help to stop this problem. The findings of Nishitani et al [12]. showed that strict government policies on the environment can reduce greenwashing. Consequently, Nemes et al. dedicated their research to creating a model that serves as a valuable guideline for assessing the environmental transparency of companies and outlining various approaches to halting the spread of greenwashing [13]. What's more, de Silva Lokuwaduge and De Silva thought that a worldwide set of rules would make it easier to check the information about the environment and make it the same for everyone [14]. In turn, it was considered by Verma and Bharti that companies can be held accountable for false claims if a robust legislative framework is implemented [15].

Furthermore, Li and his team said that in the short term, making rules about the environment and writing bad things about companies might help to stop greenwashing [16]. By contrast, Zhang believed that environmental rules could enhance the standard of goods and services provided by companies with minimal pollution only. In turn, Sun and Zhang found that government regulations, specifically government punishment contribute to greenwashing in deterring heterogeneous companies [17]. In addition, Arouri et al. introduced the level of environmental costs, which affect product market competition, as a new element able to curb greenwashing [18]. More recently, far from developing greenwashing issues, Awdek demonstrated the notable role of government effectiveness and strong regulation in enhancing environmental quality. Furthermore, Kim and Lyon contended that the magnitude of greenwashing is dictated by the oversight of non-profit organizations [19]. The development of a new regulatory instrument capable of mitigating the propagation of greenwashing is a task for which a collaboration is required between the government and stakeholders. In contrast, Lee et al. overlooked the part played by government environmental policies. Instead, they thought that greenwashing practices might actually encourage firms to adopt genuine green behavior.

A company's image and credibility can be damaged by even minor discrepancies between its environmental claims and its actual practices. Research in the Public Relations Review found that any level of greenwashing diminishes public perception of a company's integrity, highlighting the critical importance of honesty in corporate social responsibility initiatives [20].

Investors are increasingly wary of greenwashing, as it signals potential ethical and operational risks. A systematic literature review in Management Review Quarterly highlighted that the greenwashing practices deter investment and can negatively impact a company's financial performance. This is due to the perceived dishonesty and the potential for future regulatory penalties associated with misleading environmental claims [21].

Greenwashing adversely affects internal stakeholders, particularly employees. A study in Business Strategy and the Environment revealed that employees who perceive their company as engaging in greenwashing are more likely to view the organization as hypocritical, leading to increased turnover intentions. This effect is especially pronounced among employees with environmental education, indicating that greenwashing can result in the loss of valuable, environmentally conscious staff [22].

Greenwashing significantly erodes consumer trust, leading to negative brand perceptions. A study published in the Journal of Retailing and Consumer Services demonstrated that greenwashing fosters brand hate and perceptions of hypocrisy, which in turn drive consumers to avoid the brand and engage in negative word-of-mouth. This underscores the necessity for authentic and transparent environmental communications [23].

Uncertainty over the introduction of carbon pricing gives rise to transition risk. We demonstrate that green bonds exhibit a price premium over conventional bonds in circumstances characterized by information asymmetry, transition risk, and the imposition of substantial costs in the event of greenwashing, that is, the presentation of false or exaggerated claims pertaining to the green nature of a given entity. The extent of greenwashing in the market is a function of the green bond premium, which is a measure of the cost of financing environmental projects. If carbon pricing is introduced quickly and in a gradual way, it will cause a small increase in the price of green bonds and a low level of greenwashing. On the other hand, if it is delayed and the price of carbon is increased quickly, the effect on both is unclear [24].

3. Methodology

3.1. Data collection and processing

This paper uses an event study as a method to prove the hypothesis, which can help quantify unusual changes in stock prices when a particular event occurs, such as when a company is exposed for greenwashing practices. This method can reveal the market's reaction to an event by comparing stock price movements before and after the event.

Data sources are from Investing.com, which are the stock price in Volkswagen and S&P 500. The expected return rate of Volkswagen was derived through the regression analysis of the investment returns of S&P 500 and Volkswagen. This website has diverse data, provided by the world's leading financial market data providers and exchanges. It is widely used by investors, analysts, researchers and financial practitioners worldwide. The platform has a high frequency of data updates. Using Excel to calculate the value that is needed. Because it's a quick and easy way to discover price changes in stock prices.

By setting the Event Window [-10, +10], distinguish the market performance before and after the event to analyze the data method. Smooth out short-term fluctuations caused by non-event factors to ensure that the abnormal return (AR) is actually due to the event and not the normal volatility of the market. Selecting price data for the first 252 days of the event window. 252 days, representing a full trading year, is a common standard used empirically to ensure that the results of event studies have a certain degree of reliability and generality.

First of all, calculate the individual Stock Return by S&P 500 and Volkswagen.

The intercept, slope, R-square and standard error are then calculated using the historical data regression of Volkswagen and S&P 500 return (Table 1).

|

intercept |

0.000487677 |

|

slope |

0.336995123 |

|

R-square |

0.023042888 |

|

Standard Error |

0.016840728 |

In order to get an abnormal return (AR), need to first estimate the "normal" return when no event occurs. In general, a regression model can be used to estimate normal returns.

After that, then calculate abnormal return.

To measure the overall impact of the event, add all of the abnormal returns to get Cumulative Abnormal Return (CAR).

Last but not least, Table 2 can be received.

|

Data of R/AR/CAR |

||

|

R-expect return |

AR-abnormal return |

CAR-cumulative abnormal return |

|

-0.000482745 |

0.009013803 |

0.009013803 |

|

0.004802305 |

0.004185271 |

0.013199074 |

|

-0.002731409 |

-0.034208596 |

-0.021009521 |

|

0.000811073 |

-0.033455252 |

-0.054464773 |

|

5.15107E-05 |

0.003604282 |

-0.050860491 |

|

0.001797872 |

0.000443652 |

-0.050416839 |

|

0.002243951 |

-0.007276101 |

-0.05769294 |

|

-0.000393922 |

-0.007473457 |

-0.065166397 |

|

-0.002292625 |

-0.016398964 |

-0.08156536 |

|

-0.006626232 |

-0.015018789 |

-0.09658415 |

|

-0.010239485 |

-0.004804763 |

-0.101388912 |

|

-0.012797888 |

-0.030628287 |

-0.1320172 |

|

-0.004069198 |

0.062929561 |

-0.069087639 |

|

0.013641963 |

-0.018372892 |

-0.08746053 |

|

0.008684621 |

0.014488284 |

-0.072972246 |

|

0.000691125 |

-0.005627246 |

-0.078599492 |

|

-0.002341937 |

-0.008454679 |

-0.087054171 |

|

-0.009491288 |

-0.020892193 |

-0.107946363 |

|

0.006668328 |

-0.014882505 |

-0.122828868 |

|

0.000868091 |

0.021831295 |

-0.100997573 |

|

-0.004676668 |

-0.022317933 |

-0.123315506 |

At the end, calculate AR t-test. The t value is -0.285306128.

272 days of stock prices were collected, so the degree of freedom is 271. With a single-tailed test and a significance level of 0.05, a critical value of about 1.645 can be obtained. The t value is -0.285306128, which is negative and less than the critical value of 1.645, so the H0 cannot be rejected. Greenwashing would harm the financial performance of companies.

3.2. Results

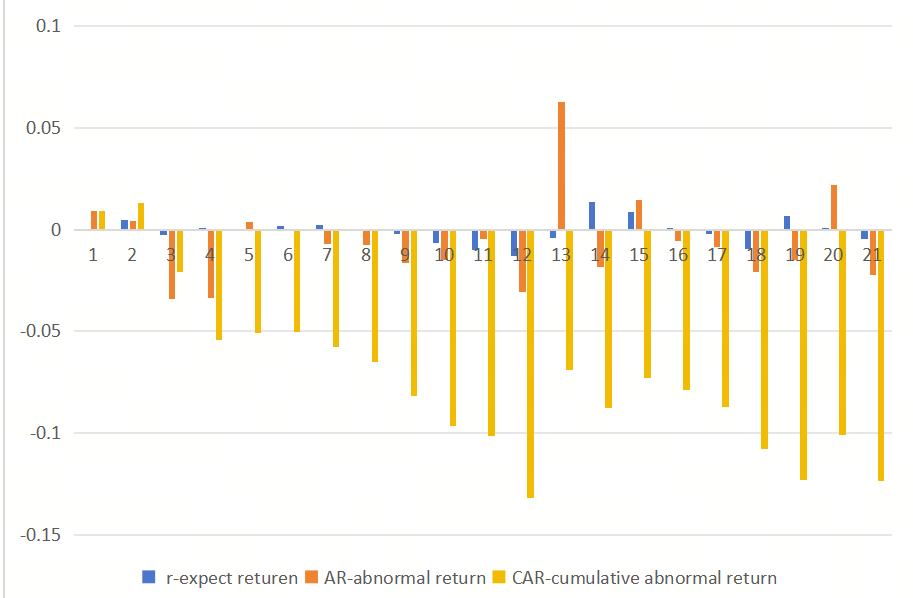

From the provided data, it can be observed that the abnormal returns (AR) show significant fluctuations during the event window, especially around the event date, August 21, 2015. Before the days Volkswagen had announced greenwashing, the number of AR and CAR was fairly smooth. On the day of August 21, the number reduced dramatically. From August 21 to August 24, Volkswagen's stock price did not recover immediately. Abnormal returns remain in negative territory most of the time, indicating that the market's reaction to events persists. After August 24, abnormal returns are still volatile; some signs of recovery are beginning to appear. But the general trend of CAR was still negative and decreased (Figure 1).

4. Conclusion

In summary, the announcement of greenwashing, had a negative impact on Volkswagen’s stock, and this effect was captured by the abnormal returns during the event window. It maybe because of the decrease of Volkswagen’s reputation among the public. Although share prices recovered slightly a few days later, the market did not recover immediately. The market is beginning to digest the impact of the event, but the process is slow. It also showed that being declared greenwashing had had a profound negative effect on the company.

This reaction is also related to the social theory named Stakeholder Theory. Freeman [25] states that a firm’s success depends on its relationships with multiple stakeholders, not just shareholders. The negative market reaction of Volkswagen suggested that stakeholders (investors, customers, and regulators) punished Volkswagen for unethical practices. Even if short-term financial recovery occurs, long-term trust damage may affect customer loyalty, regulatory scrutiny, and investment attractiveness.

The drawback of this paper lies in the lack of more analysis on the stock prices of various companies. Because ESG has only become widely known to the public in recent years, the available data samples that can be found online are rather limited. Meanwhile, among the companies that are known to have engaged in greenwashing, the number is extremely small. This has made it difficult to search for relevant data. However, as people's awareness of the environment keeps increasing, the issue of greenwashing will be given more and more attention, and this is just the beginning.

References

[1]. Zhou, D., Kythreotis, A. (2024) Why issue green bonds? Examining their dual impact on environmental protection and economic benefits. Humanit Soc Sci Commun 11, 1761.

[2]. Ren X., Zeng G., Sun X. (2023) The peer effect of digital transformation and corporate environmental performance: Empirical evidence from listed companies in China. Economic Model. 128: 106515.

[3]. Simionescu M., Gavurová B. (2023) Pollution, income inequality and green finance in the new EU member states. Humanities and Social Sciences Communications, 10(1).

[4]. Zhou X.G., Tang X.M., Zhang R. (2020) Impact of green finance on economic development and environmental quality: a study based on provincial panel data from China. Environ. Sci. Pollut. Res. 27(16): 19915–19932.

[5]. Walker K., Wan F. (2012) The harm of symbolic actions and green-washing: corporate actions and communications on environmental performance and their financial implications. J. Bus. Ethics 109(2): 227–242.

[6]. Nyilasy G., Gangadharbatla H., Paladino A. (2014) Perceived greenwashing: the interactive effects of green advertising and corporate environmental performance on consumer reactions. J. Bus. Ethics 125(4): 693–707.

[7]. Adam Hayes. (2024) Greenwashing: Definition, How It Works, Examples, and Statistics https: //www.investopedia.com/terms/g/greenwashing.asp

[8]. Bernini F., La Rosa F. (2024) Research in the greenwashing field: concepts, theories, and potential impacts on economic and social value. J Manag Gov, (28): 405–444.

[9]. Feghali, K., Najem, R., Metcalfe, B. D. (2025). Greenwashing in the era of sustainability: A systematic literature review. Corporate Governance and Sustainability Review, 9(1): 18–31.

[10]. Lyon, T. P., Montgomery, A. W. (2015). The means and end of greenwash. Organization & Environment, 28(2): 223–249.

[11]. Xianwang Shi, Jianteng Ma, Anxuan Jiang, Shuang Wei, Leilei Yue. (2023) Green bonds: green investments or greenwashing? https: //www.sciencedirect.com/science/article/abs/pii/S1057521923003666

[12]. Free, C., Jones, S., Tremblay, M.S. (2024). Greenwashing and sustainability assurance: A review and call for future research. Journal of Accounting Literature.

[13]. Nemes, N., et al. (2022). An Integrated Framework to Assess Greenwashing. Sustainability, 14(8): 4431.

[14]. de Silva Lokuwaduge, C. S., De Silva, K. M. (2022). ESG Risk Disclosure and the Risk of Green Washing. Australasian Accounting, Business and Finance Journal, 16(1): 146–159.

[15]. Verma, M., Bharti, U. (2023). Combating Greenwashing Tactics and Embracing the Economic Success of Sustainability. VEETHIKA: An International Interdisciplinary Research Journal, 9(3): 9–16.

[16]. Li, Z., et al. (2023). How Does Environmental Regulation Affect Corporate Environmental, Social, and Governance (ESG) Greenwashing? Evidence from China. Sustainability, 16(23), 10608.

[17]. Sun, Y., Zhang, Y. (2019). Greenwashing Risks in Environmental Quality Competition: Detection and Deterrence. Games, 10(2), 14.

[18]. Arouri, M., El Ghoul, S., Gomes, M. (2021). Greenwashing and Product Market Competition. Finance Research Letters, 42, 101927.

[19]. Kim, E. H., Lyon, T. P. (2015). Greenwash vs. Brownwash: Exaggeration and Undue Modesty in Corporate Sustainability Disclosure. Organization Science, 26(3): 705–723.

[20]. Keilmann, J., Koch, T. (2023). When Environmental Claims are Empty Promises: How Greenwashing Affects Corporate Reputation and Credibility. Environmental Communication, 18(3): 266–284.

[21]. Gatti, L., Seele, P., Rademacher, L. (2023). A systematic literature review on greenwashing and its relationship to stakeholders: State of art and future research agenda. Management Review Quarterly, 74(1), 1397–1421.

[22]. Robertson, J. L., Montgomery, A. W., Ozbilir, T. (2023). Employees' response to corporate greenwashing. Business Strategy and the Environment, 32(7): 4015–4027.

[23]. Sajid, M., Zakkariya, K. A., Suki, N. M., Islam, J. U. (2024). When going green goes wrong: The effects of greenwashing on brand avoidance and negative word-of-mouth. Journal of Retailing and Consumer Services, 78, 103773.

[24]. Chen, Z., Qian, C. (2023). Green Bond Pricing and Greenwashing under Asymmetric Information. SSRN Working Paper.

[25]. University virginia | Darden School of Business. The Past, Present and Future of Stakeholder Theory. https: //www.darden.virginia.edu/stakeholder-theory

Cite this article

You,Y. (2025). Analysis of the Impact of Greenwashing on Stock Financial Performances of Companies. Advances in Economics, Management and Political Sciences,203,57-63.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Volume title: Proceedings of ICEMGD 2025 Symposium: Resilient Business Strategies in Global Markets

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Zhou, D., Kythreotis, A. (2024) Why issue green bonds? Examining their dual impact on environmental protection and economic benefits. Humanit Soc Sci Commun 11, 1761.

[2]. Ren X., Zeng G., Sun X. (2023) The peer effect of digital transformation and corporate environmental performance: Empirical evidence from listed companies in China. Economic Model. 128: 106515.

[3]. Simionescu M., Gavurová B. (2023) Pollution, income inequality and green finance in the new EU member states. Humanities and Social Sciences Communications, 10(1).

[4]. Zhou X.G., Tang X.M., Zhang R. (2020) Impact of green finance on economic development and environmental quality: a study based on provincial panel data from China. Environ. Sci. Pollut. Res. 27(16): 19915–19932.

[5]. Walker K., Wan F. (2012) The harm of symbolic actions and green-washing: corporate actions and communications on environmental performance and their financial implications. J. Bus. Ethics 109(2): 227–242.

[6]. Nyilasy G., Gangadharbatla H., Paladino A. (2014) Perceived greenwashing: the interactive effects of green advertising and corporate environmental performance on consumer reactions. J. Bus. Ethics 125(4): 693–707.

[7]. Adam Hayes. (2024) Greenwashing: Definition, How It Works, Examples, and Statistics https: //www.investopedia.com/terms/g/greenwashing.asp

[8]. Bernini F., La Rosa F. (2024) Research in the greenwashing field: concepts, theories, and potential impacts on economic and social value. J Manag Gov, (28): 405–444.

[9]. Feghali, K., Najem, R., Metcalfe, B. D. (2025). Greenwashing in the era of sustainability: A systematic literature review. Corporate Governance and Sustainability Review, 9(1): 18–31.

[10]. Lyon, T. P., Montgomery, A. W. (2015). The means and end of greenwash. Organization & Environment, 28(2): 223–249.

[11]. Xianwang Shi, Jianteng Ma, Anxuan Jiang, Shuang Wei, Leilei Yue. (2023) Green bonds: green investments or greenwashing? https: //www.sciencedirect.com/science/article/abs/pii/S1057521923003666

[12]. Free, C., Jones, S., Tremblay, M.S. (2024). Greenwashing and sustainability assurance: A review and call for future research. Journal of Accounting Literature.

[13]. Nemes, N., et al. (2022). An Integrated Framework to Assess Greenwashing. Sustainability, 14(8): 4431.

[14]. de Silva Lokuwaduge, C. S., De Silva, K. M. (2022). ESG Risk Disclosure and the Risk of Green Washing. Australasian Accounting, Business and Finance Journal, 16(1): 146–159.

[15]. Verma, M., Bharti, U. (2023). Combating Greenwashing Tactics and Embracing the Economic Success of Sustainability. VEETHIKA: An International Interdisciplinary Research Journal, 9(3): 9–16.

[16]. Li, Z., et al. (2023). How Does Environmental Regulation Affect Corporate Environmental, Social, and Governance (ESG) Greenwashing? Evidence from China. Sustainability, 16(23), 10608.

[17]. Sun, Y., Zhang, Y. (2019). Greenwashing Risks in Environmental Quality Competition: Detection and Deterrence. Games, 10(2), 14.

[18]. Arouri, M., El Ghoul, S., Gomes, M. (2021). Greenwashing and Product Market Competition. Finance Research Letters, 42, 101927.

[19]. Kim, E. H., Lyon, T. P. (2015). Greenwash vs. Brownwash: Exaggeration and Undue Modesty in Corporate Sustainability Disclosure. Organization Science, 26(3): 705–723.

[20]. Keilmann, J., Koch, T. (2023). When Environmental Claims are Empty Promises: How Greenwashing Affects Corporate Reputation and Credibility. Environmental Communication, 18(3): 266–284.

[21]. Gatti, L., Seele, P., Rademacher, L. (2023). A systematic literature review on greenwashing and its relationship to stakeholders: State of art and future research agenda. Management Review Quarterly, 74(1), 1397–1421.

[22]. Robertson, J. L., Montgomery, A. W., Ozbilir, T. (2023). Employees' response to corporate greenwashing. Business Strategy and the Environment, 32(7): 4015–4027.

[23]. Sajid, M., Zakkariya, K. A., Suki, N. M., Islam, J. U. (2024). When going green goes wrong: The effects of greenwashing on brand avoidance and negative word-of-mouth. Journal of Retailing and Consumer Services, 78, 103773.

[24]. Chen, Z., Qian, C. (2023). Green Bond Pricing and Greenwashing under Asymmetric Information. SSRN Working Paper.

[25]. University virginia | Darden School of Business. The Past, Present and Future of Stakeholder Theory. https: //www.darden.virginia.edu/stakeholder-theory