1. Introduction

For more than 30 years, Japan, the United States, and Spain have all undergone financial crises precipitated by the collapse of asset price bubbles. All three countries exposed the shortcomings of monetary policy in addressing systemic financial risks and maintaining financial stability. According to Tinbergen’s rule, the number of policy instruments must be at least equal to the number of targets. The central bank's previous monetary policy mainly aimed at price stability, thus lacks the policy tools to maintain financial stability. Although the concept of macroprudential was introduced as early as 1979, central banks in developed countries realized that they lacked effective tools to deal with systemic financial risks after the financial crisis in 2008. With the introduction of Basel III, advanced economies began to combine monetary policy with macro-prudential policy to alleviate the difficulties caused by the implementation of a single policy. Markus, Simon, and Isabel argue that if an asset price bubble bursts, it could trigger a systemic financial crisis, the extent of which depends on the financial system. At the same time, this further illustrates the inability of macroeconomic policies to deal with asset price bubbles. Macroprudential policy regulation is optimal during economic booms because systemic risks show signs of rising as early as the boom period, but this measure is difficult to implement during the boom period [1].

Scott, Satish, and Janusz emphasize that the global financial crisis has led to systemic financial risks and the importance of central banks supervising the financial system, after all the crisis was a manifestation of the fragility of the financial system. Indeed, policymakers need to recognize the importance of macroprudential policy regulation in maintaining financial stability. If the government only adopts micro-prudential regulation, policymakers will focus on individual industries or institutions and implement targeted policies for them, but other institutions will be affected by negative policy shocks, which will cause volatility in the entire financial market [2]. Ozge and Jane argue that, in the aftermath of the global financial crisis, both developed and emerging economies have adopted macroprudential policies more frequently, tightening more than easing. Macroprudential policies in developed and emerging economies should mainly be used to deal with real estate overheating. And macroprudential changes generally follow the same pattern as changes in bank reserve ratios, capital flow management, and monetary policy. Macroprudential policy measures for the management of capital flows will have an impact on credit growth, and then play a role in restraining the rapid growth of credit and housing prices [3]. So, does the "dual-pillar policy" play an important role in preventing systemic risks and maintaining financial stability for a country? Therefore, the second part of this paper describes the consequences of the lack of macroprudential policies using the bubbles in Japan, the United States, and Spain as examples; the third part analyzes the short-term interest rates in Japan, the interbank lending rates in the United States and Spain, as well as the housing price index (2015=100) and the GDP growth rates of all three of them to derive the responses of the three countries in the event of a bubble-induced financial crisis brought about by loose monetary policy; and the last part reiterates the importance of macroprudential policies and summarize the implications for macroprudential regulation in China.

2. Literature review

2.1. Japan

Takatoshi found that after decades of boom and bust, the bursting of the bubble caused by Japan's financial crisis led to a prolonged period of economic stagnation since the 1990s. Especially after the signing of the Plaza Accord, Japan adopted a loose monetary policy for a long period when the economy was in good shape, which led to the creation of a bubble. In 1992, excessive investment in Japan's real estate sector (asset price bubbles) led to the problem of non-performing loans. The Japanese government missed the opportunity to rescue the economy by not tightening policy at this time, which not only burst the housing bubble but also threw the financial system into turmoil. It may also be that the Japanese government believes that its strong GDP position is sufficient to resist the economic volatility that follows policymakers who prick bubbles. As a result, the Japanese at that time believed that the bursting of the bubble was the main cause of economic stagnation, without considering whether it was a lack of financial regulation [4].

Yang and Les also emphasized that the main features of the asset price bubble in Japan were rising asset prices, overheated economic activity, and inflated money and credit supply. Although three decades had passed, the real estate market had not recovered to the heights of the boom period, and government debt had continued to increase. Japan had the title of “lost decade” in the 1990s, which implied that the Japanese economy would be in a state of stagnation in the coming decade. The asset price bubble in Japan in the 1980s and 1990s was arguably one of the worst financial bubbles in history, and at the time, the Japanese believed that rising asset prices had more to do with economic fundamentals than with irrational real estate exuberance [5].

2.2. The U.S.

The U.S. housing market bubble peaked in the 1970s and 1980s, and home prices began to rise in the late 1990s, which can be attributed to rising incomes. This lasted until 2006, after which prices began to fall. Steven and Smith argue that the failure of banks that owned securities made the U.S. financial system much less creditworthy. However, when home prices began to plummet, many people with little income and assets began to default on their loans, and banks were unable to obtain loans from these peer institutions that had been involved in many of the subprime mortgage investments. However, as credit became increasingly difficult to obtain, the U.S. subprime mortgage crisis occurred in 2008. Companies like Lehman Brothers and Bear Stearns, which were caught in the burst of the real estate bubble, collapsed as a result of the expansion of credit brought about by the United States’ easy monetary policy, the Federal Reserve's tardiness in tightening monetary policy, and the failure of many firms to recognize the real estate market's weakness and balance their exposures [6].

Pablo A. Guerron-Quintana, Tomohiro Hirano, and Ryo Jinnai argued that the recovery from crises occurred after the bursting of bubbles was much slower than that of a general recession, which coincided with Brunnermeier and Oehmke's view that crises led to economic contraction. Asset price bubble bursts were not uncommon but were repeated over time. At the same time, there was a large and unfavorable financial shock in the 2008 financial crisis, which could further explain the bursting of the United States housing bubble. On the other hand, Pablo A. Guerron-Quintana, Tomohiro Hirano, and Ryo Jinnai feel that if the equilibrium in the United States had been in a different state, for example, without bubbles, the U.S. economy would have grown very fast in the long run [7].

2.3. Spain

Since Spain joined the European Monetary Union in 1999, the Spanish economy has begun to prosper, and monetary policy, mainly the expansionary loose monetary policy and low-interest rate policy implemented by the European Central Bank, has led to a massive inflow of capital into Spain, which has boosted the real estate boom in Spain, and the credit market has begun to be deregulated. At the same time, house prices began to rise and the role of the credit channel gradually took over [8]. Alberto, Enrique, and Tom argue that the rise in demand for housing credit increased bank profits and net worth. The relaxation of bank lending standards and the speculative bubble in house prices may have been an incentive for the Spanish boom to attract Spanish banks to increase housing credit, while at the same time, the real estate boom initially slowed down but eventually stimulated the growth of non-housing credit as well [9]. However, while Spain’s monetary policy brought about the boom, the excesses of the boom also brought about the bubble [8].

Alberto, Enrique, and Tom argued that when the real estate bubble appeared, they became rich and the demand for bank credit increased, and banks were unable to increase the supply of credit. However, the bubble bursting led to a reduction in the amount of loans that should have been repaid to the banks, triggering a credit crunch. Spain began to experience a prolonged recession after the financial crisis of 2008, and house prices began to fall at a time when there was almost no new construction, and there was a massive inflow of capital. The analysis by Alberto et al. shows that the growing demand for housing credit in Spain squeezed non-housing credit and that the growing demand for non-housing credit was not sufficient to meet the growing demand for housing credit in Spain. Bubble mortgages also increased bank net worth and the availability of credit in all sectors. Thus, it can be argued that the boom-to-bust process in Spain was essentially the same as the theoretical predictions of Alberto et al [10]..

By analyzing the lessons learned from Japan, the United States, and Spain, they all adopted loose monetary policies. When the real estate bubble (asset price bubble) appeared, Japan and Spain did not regulate it promptly, but allowed it to continue to spread. At the same time, these two countries began to try to save the economy by tightening the monetary policy only after they realized the problem, but it was too late, which ultimately led to the bursting of the bubble, the downturn of the economy and the financial crisis. However, although the United States also encountered the bubble problem in the 2008 financial crisis, the United States used macroprudential policies to save the United States economy in time after the crisis to avoid being held hostage by the Lehman Brothers, which was too big to fail. Therefore, the United States avoided embarking on the same path as Japan and Spain. This further illustrates the importance of monetary policy and macroprudential policy (dual-pillar policy), both of which are indispensable. Although some emerging economies had used macroprudential policies before the crisis, they only made extensive use of macroprudential policies in the years following the 2008 crisis. Thus, this may indicate that the macroprudential framework is crisis-driven and that only effective macroprudential policies can compensate for the shortcomings of monetary policy [11].

3. Methodology

3.1. Data

For Japanese data, this paper searches the OECD database for the housing price index (2015 is the base year) and short-term interest rate data from 1980 to 2020, which is not enough to prove for Japan the effect of its loose monetary policy on interest rates and real estate, as Japanese interbank lending rate data is counted from 2003. After that, this study searches the World Bank database for Japan’s GDP growth data from 1980 to 2020. Regarding the data for the United States, this study first uses the OECD database as a data source. In this database, U.S. interbank lending rates are searched from 1980 to 2020 and used as a proxy for short-term nominal interest rates. Then, housing price index data are also searched from 1980 to 2020 with 2015 as the base year. The study then searches the World Bank database for U.S. GDP growth rate data from 1980 to 2020. Next, for the case of Spain, this study searches both databases for the Spanish Interbank Lending Rate (which also represents the short-term nominal interest rates), the House Price Index (using 2015 as the base year), and the GDP growth rate for the same years. By comparing the data of the three countries, further evidence can ultimately be presented that their long period of loose monetary policy led to the bursting of the bubble and the financial crisis. At the same time, this can also conclude the attitude of the three of them when they encountered this situation. The study presents data on short-term interest rates, house price indices, and GDP growth rates for the three countries in line graphs.

3.2. Results

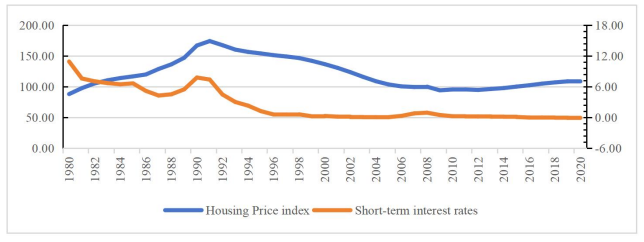

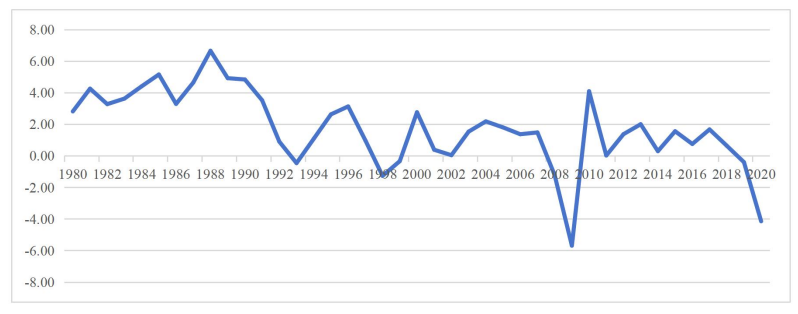

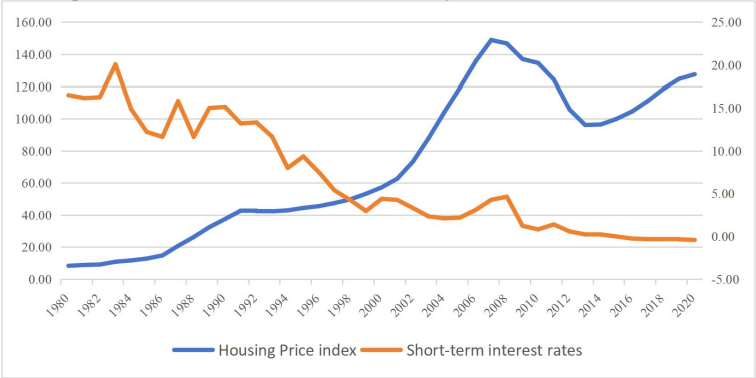

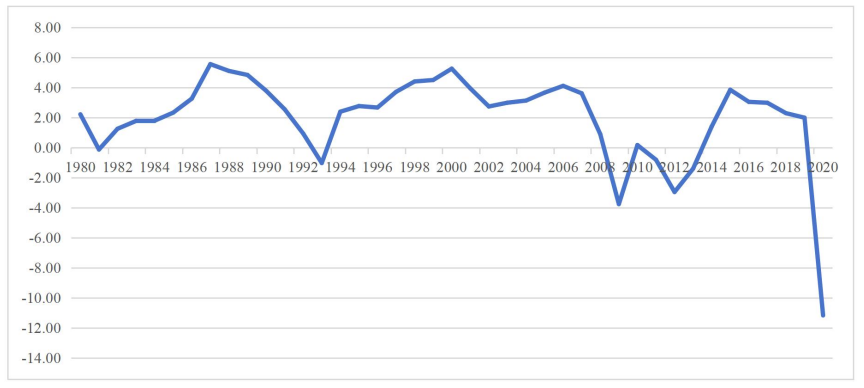

Figure 1 and Figure 2 show Japan’s short-term interest rates, house price index, and Japan’s GDP growth rate. It is easy to see that since the early 1990s, Japan's house prices have been consistently high, while interest rates have been consistently low, and although they increased in 1990, they began to decrease gradually in the following years. Meanwhile, Japan’s GDP growth rate declined rapidly from 6% in 1988 to 1.5% on average in the 1990s and even turned negative. This shows that Japan had been pursuing an easy monetary policy in the 1990s, and instead of implementing macro-prudential policies to regulate the situation, it allowed the bubble to develop. Thereafter, Japan fell into a liquidity trap, which led to the eventual bursting of the bubble.

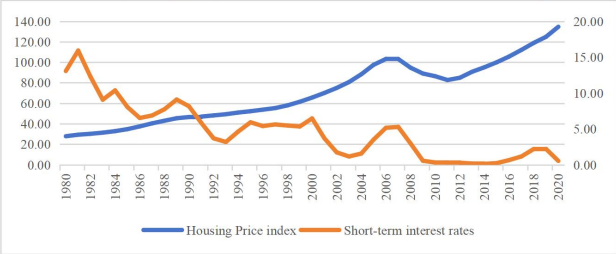

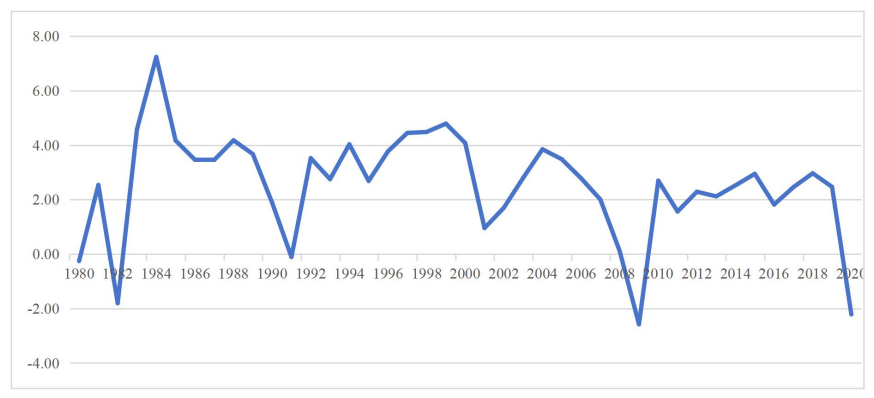

Figure 3 and Figure 4 depict trends in short-term interest rates, house price indices, and GDP in the United States, respectively. In 2006, house prices fell and interest rates rose in the United States; after the 2008 crisis, house prices started to decline and short-term interest rates fell. At the same time, from 2006 to 2008 (after the financial crisis), the GDP growth rate of the United States began to decline and even reached a negative value in 2009, which means that the economic growth of the United States began to slow down. However, after 2010, GDP growth in the US began to rise. Thus, although the United States was also hit by the financial crisis caused by the bursting of the real estate bubble and the subprime mortgage crisis in 2008, the timely implementation of macroprudential policies saved the United States economy.

Figure 5 and Figure 6 show short-term interest rates, house price indices and GDP growth rates for Spain. From these two graphs, we can conclude that at the beginning of the 21st century, with Spain’s accession to the European Union and the easy monetary policy of the European Central Bank, the Spanish economy was booming, house prices were rising and interest rates were falling. However, in 2008, Spanish house prices began to fall and interest rates rose in the same year. In terms of GDP growth, Spain’s GDP growth rate has fluctuated and was even negative in 2009. However, the failure to implement timely macroprudential policies in 2008 led to the bursting of the Spanish real estate bubble and the downward spiral of the Spanish economy, triggering the impact of the financial crisis on Spain. Although the situation in Spain changed in the following years, the changes were not significant.

The US central bank’s effective response to the subprime crisis benefited from the introduction of a macroprudential policy framework for countries under the Basel III agreement. However, to circumvent Basel III, commercial banks transformed their risks through different markets that relied on different regulations, thus allowing for unrestricted increases in bank leverage. The financial depth, openness, and liberalization of developed countries are far greater than those of emerging economies. Advanced economies such as the United States have the flexibility to choose between monetary and macroprudential policies during booms and recessions, but they will also face more complex financial innovations created by commercial banks to evade Basel III regulations.

For developing countries like China and emerging economies, the regulatory performance of the “dual-pillar policy” is not very impressive compared with that of developed economies due to the constraints of insufficient macroprudential policy effectiveness. Therefore, the implementation of macroprudential policies in emerging economies needs to be assessed in terms of the macroprudential effectiveness framework with specific national conditions as the entry point. At the same time, it is also important to grasp the regulatory strength of the “dual-pillar” policy to avoid policy conflicts. Finally, emerging economies must first understand the shortcomings in the policy transmission process and use them to improve macroprudential policies suitable for developing countries.

4. Conclusion

This paper explains the importance of “dual-pillar policies” by examining the lessons learned from the financial crises in Japan, the United States, and Spain. By comparing the macro policy control during the real estate bubble in the three countries, it is found that after the financial crisis caused by the bubble burst, the "dual-pillar" adjustment, which combines macro-prudential policies and loose monetary policies, could save the economy as in the United States. Loose monetary policy alone could not save Japan and Spain during the recession. The depth, openness, and liberalization of emerging economies’ financial markets are far less than those of developed countries, which prevents them from copying exactly from developed countries in the use of macro-prudential tools. For emerging economies, such as China, the independence of the central bank should be ensured first and gradually carry out market-oriented interest rate and exchange rate reform. Although this paper only analyzes the causes of financial crises in three developed countries and the importance of the “dual-pillar” policy, it has not used empirical research to analyze the role of macroprudential policy in smoothing economic fluctuations. Future research will combine the classic and the latest research literature to improve the theoretical study and empirical analysis of this problem.

References

[1]. Brunnermeier, M., Rother, S., & Schnabel, I. (2020). Asset price bubbles and systemic risk. The Review of Financial Studies, 33(9): 4272-4317.

[2]. Ellis, S., Sharma, S., & Brzeszczyński, J. (2022). Systemic risk measures and regulatory challenges. Journal of Financial Stability, 61, 100960.

[3]. Akinci, O., & Olmstead-Rumsey, J. (2018). How effective are macroprudential policies? An empirical investigation. Journal of Financial Intermediation, 33, 33-57.

[4]. Ito, T. (2003). Retrospective on the Bubble Period and Its Relationship to Developments in the 1990s. World Economy, 26(3): 283-300.

[5]. Hu, Y., & Oxley, L. (2018). Bubble contagion: Evidence from Japan’s asset price bubble of the 1980-90s. Journal of the Japanese and International Economies, 50, 89-95.

[6]. Gjerstad, S., & Smith, V. L. (2009). Monetary policy, credit extension, and housing bubbles: 2008 and 1929. Critical Review, 21(2-3): 269-300.

[7]. Guerron-Quintana, P. A., Hirano, T., & Jinnai, R. (2023). Bubbles, crashes, and economic growth: Theory and evidence. American Economic Journal: Macroeconomics, 15(2): 333-371.

[8]. Pál, T. (2018). The effects of monetary policy on house prices in Spain: the role of the economic and monetary union membership in the housing bubble prior to the great recession. The Central European Review of Economics and Management (CEREM), 2(2): 5-40.

[9]. Martín, A., Moral-Benito, E., & Schmitz, T. (2021). The financial transmission of housing booms: evidence from Spain. American Economic Review, 111(3): 1013-1053.

[10]. Martin, A., Moral-Benito, E., & Schmitz, T. (2018). The financial transmission of housing bubbles: Evidence from Spain. Documentos de Trabajo/Banco de España, 1823.

[11]. IMF, F. (2016) BIS: Elements of Effective Macroprudential Policies. Lessons from International Experience, International Monetary Fund, Financial Stability Board, Bank for International Settlements, 31 August.

Cite this article

Dong,R.;Dong,Y. (2025). Analysis of the “Dual-Pillar Policy”–Based on Lessons Learned from Japan, the United States and Spain. Advances in Economics, Management and Political Sciences,208,24-31.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Volume title: Proceedings of ICFTBA 2025 Symposium: Financial Framework's Role in Economics and Management of Human-Centered Development

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Brunnermeier, M., Rother, S., & Schnabel, I. (2020). Asset price bubbles and systemic risk. The Review of Financial Studies, 33(9): 4272-4317.

[2]. Ellis, S., Sharma, S., & Brzeszczyński, J. (2022). Systemic risk measures and regulatory challenges. Journal of Financial Stability, 61, 100960.

[3]. Akinci, O., & Olmstead-Rumsey, J. (2018). How effective are macroprudential policies? An empirical investigation. Journal of Financial Intermediation, 33, 33-57.

[4]. Ito, T. (2003). Retrospective on the Bubble Period and Its Relationship to Developments in the 1990s. World Economy, 26(3): 283-300.

[5]. Hu, Y., & Oxley, L. (2018). Bubble contagion: Evidence from Japan’s asset price bubble of the 1980-90s. Journal of the Japanese and International Economies, 50, 89-95.

[6]. Gjerstad, S., & Smith, V. L. (2009). Monetary policy, credit extension, and housing bubbles: 2008 and 1929. Critical Review, 21(2-3): 269-300.

[7]. Guerron-Quintana, P. A., Hirano, T., & Jinnai, R. (2023). Bubbles, crashes, and economic growth: Theory and evidence. American Economic Journal: Macroeconomics, 15(2): 333-371.

[8]. Pál, T. (2018). The effects of monetary policy on house prices in Spain: the role of the economic and monetary union membership in the housing bubble prior to the great recession. The Central European Review of Economics and Management (CEREM), 2(2): 5-40.

[9]. Martín, A., Moral-Benito, E., & Schmitz, T. (2021). The financial transmission of housing booms: evidence from Spain. American Economic Review, 111(3): 1013-1053.

[10]. Martin, A., Moral-Benito, E., & Schmitz, T. (2018). The financial transmission of housing bubbles: Evidence from Spain. Documentos de Trabajo/Banco de España, 1823.

[11]. IMF, F. (2016) BIS: Elements of Effective Macroprudential Policies. Lessons from International Experience, International Monetary Fund, Financial Stability Board, Bank for International Settlements, 31 August.