1. Introduction

The evolving global corporate responsibility paradigm is forcing organizations to restructure their accountability boundaries. The traditional financial assessment system focused on shareholder interests is gradually shifting to a comprehensive assessment of environmental and social impacts. This transformation corresponds to the deepening of the concept of sustainable development, which requires companies to assume social obligations while creating economic value. The Global Reporting Initiative (GRI) Standards, as a general disclosure framework, provide companies with structured disclosure solutions for Environmental, Social, and Governance (ESG) performance. However, its voluntary nature has raised questions about its practical effectiveness—can the report's content truly reflect the demands of multiple stakeholders? How can the "dual materiality" principle be implemented—that is, simultaneously considering the impact of ESG issues on corporate financing and their adverse effects on the social environment [1]?

This study examines the effectiveness of implementing the GRI framework in terms of stakeholder inclusion and integrating dual materiality. An analysis of multinational companies' social responsibility reports reveals the advantages and limitations of the standardized disclosure system in practical applications. Case studies show that although the GRI standard has established relatively comprehensive disclosure indicators, companies still tend to selectively disclose links such as stakeholder identification and substantive issue considerations. This deviation results not only from institutional constraints but also reflects cognitive differences between different subjects regarding the connotation of sustainable development. The research findings provide empirical evidence that allows companies to optimize ESG governance and regulators to improve disclosure standards, thereby promoting the establishment of a more inclusive and substantive accountability communication mechanism.

2. Literature review

2.1. Theoretical foundation of CSR accounting

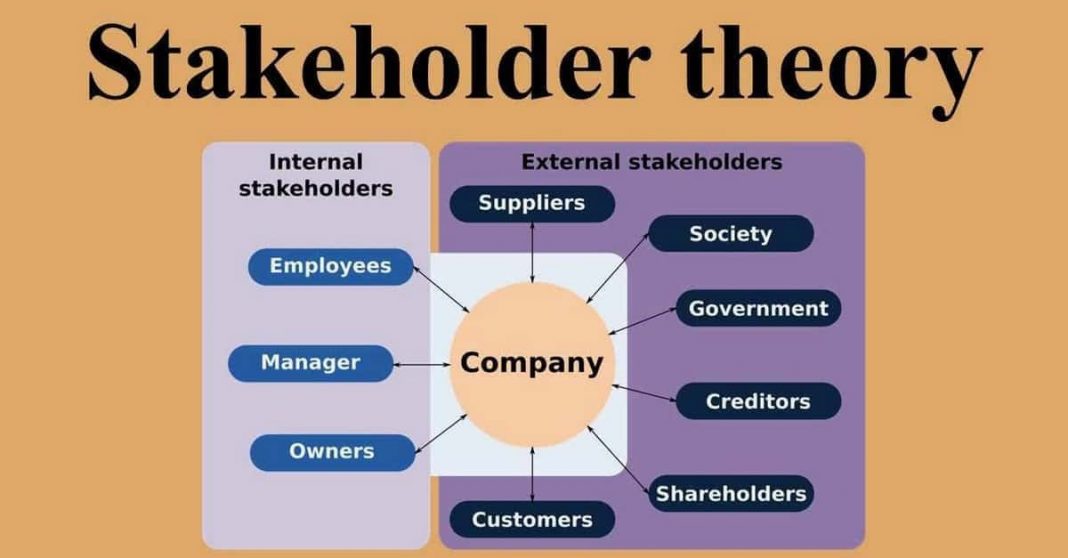

The basic concept of corporate social responsibility accounting is that the boundaries of responsibility of business organizations must transcend the traditional framework of prioritizing shareholder interests. Stakeholder theory reveals that the operation of a business involves multiple stakeholders—including internal employees, management, suppliers, as well as external consumers, communities, regulators, and so on. The decision-making process must reconcile the rights and interests of all parties. As shown in the structural model in Figure 1, stakeholders are categorized as internal employees and external partners, visually illustrating the complexity of the modern corporate responsibility system.

Legitimacy theory further explains that to achieve continued social recognition, corporate activities must comply with social value standards. Environmental Social Governance (ESG) disclosure has become a key approach. By transparently presenting practices such as energy conservation and emission reduction, and the protection of labor rights, it strengthens the foundation of trust across all sectors [2]. These two theories together build the dual value of responsible accounting: it is not only a compliance tool, but also a strategic support point for companies to maintain their reputation and achieve sustainable development in a dynamic environment. This cognitive shift leads companies to move from passive disclosure to actively building a responsible ecosystem, fulfilling social contracts while creating economic value [3].

Figure 1. Stakeholder theory framework: internal and external stakeholder groups surrounding the company (source: blog.ipleaders.in)

2.2. GRI standards and sustainability disclosure

The Global Reporting Initiative (GRI), as the authoritative framework for sustainability disclosure, has a standardized system covering a wide range of topics, from governance structure to carbon emissions measurement. Its modular reporting mechanism allows companies to adjust disclosure dimensions based on industry characteristics, which not only ensures standardized comparability of information disclosure but also meets the practical needs of different business scenarios [4]. Although the framework has consistently introduced industry-specific guidelines and advocated stakeholder dialogue, there are concerns about this from both academic and business circles—particularly the fact that companies' independent choice of participation models could weaken the practical effect, and some reports feature symbolic compliance features, rendering the disclosed content merely formalistic.

2.3. Double materiality and stakeholder-oriented reporting

The principle of dual materiality is increasingly becoming a new criterion for assessing corporate responsibility. This framework requires the simultaneous consideration of two dimensions: it is necessary to assess the impact of environmental and social factors on financial performance, and also to measure the inverse effect of the company's activities on social ecology. This two-way evaluation mechanism encourages companies to go beyond traditional risk-averse thinking and systematically review their own social footprints. This principle is linked to the stakeholder-driven disclosure path [5]. By examining substantive issues through multiple subjects, it promotes the formation of a more democratic and inclusive model of responsibility governance. Studies show that the establishment of an effective stakeholder communication mechanism has a direct impact on the accuracy of companies' identification of key issues, and thus determines the credibility and effectiveness of sustainability reporting governance [6].

3. Methodology

3.1. Research design

This study adopts a qualitative research method, combining cross-sector case comparisons and in-depth text analysis, to focus on evaluating the substantive performance of corporate reporting in terms of stakeholder communication and dual-importance integration. Unlike the indicator statistics of traditional quantitative research, this method focuses on the narrative framework of information disclosure and the argumentation logic of substantive issues, thereby revealing the true picture of corporate responsibility governance [7].

3.2. Sample selection

The research sample covers ten multinational groups in four major fields, including energy and finance. The selected companies have all adopted the GRI Standard to prepare social responsibility reports for more than three consecutive years, and their 2022-2023 annual reports have been made public. Industry diversity design allows us to observe the differences in the application of GRI Standards in different operational scenarios [8]. For example, the manufacturing industry places greater emphasis on supply chain management issues, while technology companies emphasize ethical data disclosure.

3.3. Evaluation framework

The analytical framework is built around three fundamental dimensions: the degree of implementation of the GRI Standards, the maturity of the stakeholder engagement mechanism, and the completeness of the dual-materiality mapping [9]. In addition to conventional content research, emphasis is placed on analyzing the depth of the rationale for information disclosure, including the transparency of the topic selection logic and the procedures for handling comments on stakeholder opinions [10]. At the same time, the substantive issue matrices published by each company are systematically evaluated to examine the scientific validity of their issue classification and the rationale for their prioritization.

4. Empirical analysis and process

4.1. Data collection and preprocessing

The data for the corporate social responsibility report is sourced from the company's official website and professional ESG databases. After standardizing its format, it is imported into qualitative analysis tools [11]. Non-English texts are professionally translated and verified, with a focus on self-disclosed content that exceeds legal requirements, particularly the chapters dealing with stakeholder communication and argumentation on substantive issues.

4.2. Content analysis procedure

The textual analysis focuses on three main dimensions: the stakeholder participation mechanism, the delineation of information disclosure boundaries, and the materiality assessment methodology. The details of the implementation of participation forms, such as research questionnaires and focus groups, are examined, and the depth of the description of the community opinion solicitation process is analyzed. In the substantive issues review section, emphasis is placed on distinguishing between companies that adopt a single financial impact dimension or a complex social and environmental impact assessment standard [12]. The coding process involves several rounds of cross-checking to ensure consistency in the understanding of the text's meaning by different analysts.

4.3. Comparative evaluation of GRI adoption

Cross-sector comparisons show significant differences in the implementation of the GRI Standards. Energy companies focus on disclosing carbon emissions data, manufacturing industries emphasize human rights protections in the supply chain, and technology companies strengthen issues related to data ethics and talent development [13]. However, most companies remain at the minimum level of compliance and have not established substantial stakeholder engagement mechanisms. Although innovative integrated reporting practices have emerged in some industries, the lack of mandatory requirements has led to an inequitable dissemination of information, weakening the regulatory effect that the GRI Standards are intended to have [14].

5. Results and discussion

5.1. Stakeholder inclusiveness in GRI-based reporting

The inclusive stakeholder communication mechanism advocated by the GRI framework shows a selective trend in effective implementation. The content of the reports of the ten sampled companies exhibits consistent characteristics: institutional investors (100%), regulators (90%), and customer groups (85%) receive widespread attention, while the participation of community organizations (40%), small and medium-sized suppliers (30%), and public welfare institutions (20%) is significantly insufficient (see Table 1). This structural imbalance reflects the fact that companies generally simplify stakeholder management to investor relations and compliance operations, and that their communication scope is limited by commercial interests and risk control considerations. The reports generally contain chapters on stakeholder communication, but there are significant differences in the specific details of implementation [15]. Eighty percent of companies mentioned communication forms such as questionnaires and special interviews, but did not specify how the opinions collected influenced the consideration of substantive issues. Only two companies disclosed in detail the correspondence between stakeholder requests and their ESG strategies, such as the integration of community environmental complaints into board oversight matters or the publication of rectification results of suppliers' human rights assessments. Most cases show that the communication mechanism remains at the level of describing procedures, without substantial feedback or tracking of improvements.

Table 1. Stakeholder groups covered in GRI reports

Stakeholder Group | Mentioned in Report (%) |

Investors | 100% |

Regulators | 90% |

Customers | 85% |

Employees | 75% |

Local Communities | 40% |

Small Suppliers | 30% |

Civil Society Organizations | 20% |

5.2. Integration of double materiality

The application of the principle of dual materiality in the sampled companies reveals a structural imbalance. Research data show that the coverage rate for climate change issues is 90%, energy management is 85%, and waste management is 80%, while labor rights protection is only 55%, income distribution fairness is 40%, and indigenous rights protection is 30% (see Table 2). This imbalance reflects the structural contradiction between the orientation of shareholder interests and the demand for multiple responsibilities. Companies generally implement early warning mechanisms for environmental risks, but their ability to proactively identify social issues such as human rights risks in the supply chain is relatively weak. A comparison of the report's content shows that 88% of companies disclosed in detail the calculation of the financial return on environmental protection investments, while only 32% of cases systematically assessed the long-term social benefits of community development projects. This selective disclosure leads to a deviation of the materiality assessment from the dual-dimension requirements, essentially evolving into a one-way decision-making model of "giving priority to financial materiality," which is fundamentally contrary to the balancing concept of the dual-materiality principle.

Table 2. Emphasis on environmental vs social issues in GRI reports

Issue Category | Reported with High Detail (%) |

Climate Change | 90% |

Waste Management | 80% |

Energy Efficiency | 85% |

Labor Practices | 55% |

Income Inequality | 40% |

Indigenous Rights | 30% |

6. Conclusion

This study, based on stakeholder theory and legitimacy theory, verifies the practical effectiveness of the GRI standard in corporate responsibility accounting. The research reveals that, although this framework provides methodological support for sustainable development disclosure, companies have systematic biases regarding the scope of stakeholder disclosure and the balance of dual materiality. This selective disclosure reflects the fact that most companies still view ESG reports as compliance tools rather than strategic elements. Realistic challenges such as excessive redundancy in information disclosure, fragmented regulatory standards in cross-border operations, and the priority given to reputational risk management have exacerbated the trend toward formalizing disclosed content. It is suggested that companies integrate the mechanism of stakeholder inclusion and the assessment of dual materiality into the core of their strategies. Regulatory authorities can introduce technical means such as intelligent text analysis and establish a substantive verification mechanism for disclosed content. Only by dynamically adapting corporate information disclosure to various social requirements can a transparent governance and trust mechanism truly be established in the context of sustainable development.

References

[1]. Christensen, H. B., Hail, L., & Leuz, C. (2021). Mandatory CSR and sustainability reporting: Economic analysis and literature review. European Corporate Governance Institute.

[2]. Global Reporting Initiative. (2021). The double-materiality concept: Application and issues. GRI.

[3]. Global Reporting Initiative. (2023). Double materiality: The guiding principle for sustainability reporting. GRI.

[4]. Tsang, A., Zhang, Y., & Li, Y. (2023). Environmental, social, and governance (ESG) disclosure: A literature review. The British Accounting Review, 55(1), 101149.

[5]. Deloitte. (2024). Heads Up — Unpacking the double materiality assessment under the CSRD. Deloitte.

[6]. Adams, C. A. (2021). The development and implementation of GRI standards: Practice and policy issues. In Sustainability Accounting and Accountability, 1–20. Routledge.

[7]. KPMG. (2020). The time has come: The KPMG survey of sustainability reporting 2020. KPMG International.

[8]. Cambridge Institute for Sustainability Leadership. (2023). Double materiality: Broadening corporate sustainability reporting to encompass societal and environmental impacts. University of Cambridge.

[9]. Deloitte & The Fletcher School at Tufts University. (2024). With 4 steps, sustainability disclosures can help companies earn investor trust. Deloitte.

[10]. Reuters. (2024, October 31). Companies boost social and climate reporting amid ESG backlash. Reuters.

[11]. Adams, C. A. (2021). The development and implementation of GRI standards: Practice and policy issues. In Sustainability Accounting and Accountability (pp. 1–20). Routledge.

[12]. Cambridge Institute for Sustainability Leadership. (2023). Double materiality: Broadening corporate sustainability reporting to encompass societal and environmental impacts. University of Cambridge.

[13]. Deloitte. (2024). Heads Up — Unpacking the double materiality assessment under the CSRD. Deloitte.Emerald+1

[14]. Global Reporting Initiative. (2021). The double-materiality concept: Application and issues. GRI.

[15]. Tsang, A., Zhang, Y., & Li, Y. (2023). Environmental, social, and governance (ESG) disclosure: A literature review. The British Accounting Review, 55(1), 101149. https://doi.org/10.1016/j.bar.2022.101149

Cite this article

Wan,Y. (2025). Integrating Stakeholder-Oriented Reporting and Double Materiality in CSR Accounting: A Critical Evaluation of GRI Standards in Corporate Sustainability Disclosures. Journal of Applied Economics and Policy Studies,18(5),33-37.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Journal:Journal of Applied Economics and Policy Studies

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Christensen, H. B., Hail, L., & Leuz, C. (2021). Mandatory CSR and sustainability reporting: Economic analysis and literature review. European Corporate Governance Institute.

[2]. Global Reporting Initiative. (2021). The double-materiality concept: Application and issues. GRI.

[3]. Global Reporting Initiative. (2023). Double materiality: The guiding principle for sustainability reporting. GRI.

[4]. Tsang, A., Zhang, Y., & Li, Y. (2023). Environmental, social, and governance (ESG) disclosure: A literature review. The British Accounting Review, 55(1), 101149.

[5]. Deloitte. (2024). Heads Up — Unpacking the double materiality assessment under the CSRD. Deloitte.

[6]. Adams, C. A. (2021). The development and implementation of GRI standards: Practice and policy issues. In Sustainability Accounting and Accountability, 1–20. Routledge.

[7]. KPMG. (2020). The time has come: The KPMG survey of sustainability reporting 2020. KPMG International.

[8]. Cambridge Institute for Sustainability Leadership. (2023). Double materiality: Broadening corporate sustainability reporting to encompass societal and environmental impacts. University of Cambridge.

[9]. Deloitte & The Fletcher School at Tufts University. (2024). With 4 steps, sustainability disclosures can help companies earn investor trust. Deloitte.

[10]. Reuters. (2024, October 31). Companies boost social and climate reporting amid ESG backlash. Reuters.

[11]. Adams, C. A. (2021). The development and implementation of GRI standards: Practice and policy issues. In Sustainability Accounting and Accountability (pp. 1–20). Routledge.

[12]. Cambridge Institute for Sustainability Leadership. (2023). Double materiality: Broadening corporate sustainability reporting to encompass societal and environmental impacts. University of Cambridge.

[13]. Deloitte. (2024). Heads Up — Unpacking the double materiality assessment under the CSRD. Deloitte.Emerald+1

[14]. Global Reporting Initiative. (2021). The double-materiality concept: Application and issues. GRI.

[15]. Tsang, A., Zhang, Y., & Li, Y. (2023). Environmental, social, and governance (ESG) disclosure: A literature review. The British Accounting Review, 55(1), 101149. https://doi.org/10.1016/j.bar.2022.101149