1. Introduction

In 2003, Chinese real estate industry made a significant contribution to the economy and was associated with other industries. With an average growth rate of 8.8%, real GDP growth in China is accessible from March 1992 to March 2023 and is updated on a quarterly basis. Prices for real estate were rising quickly as China's real estate market heated up. Between 1991 and 2001, the selling price of real estate increased from RMB 2,250 per square metre to RMB 1,000 per square metre [1]. Further, real estate market prices were increased by RMB 4,681 per square meter in 2009, accompanied by an annual growth rate of 10.36%. In recent eras, Chinese housing prices have reached a high stage, which includes the high cost of construction, speculative demand, and expected profit [2]. The third view belongs to the bubbles’ non-existence in the real estate market of China, such as a non-bubble theory. This theory includes China's current sustained development, real demand with increased prices, and increased housing, which denotes that there is no bubble in China's real estate market. However, the Japanese economy has suffered from increased prices in real estate and is seriously damaged, and even appeared in the "lost decade." The current study is conducted to explore and analyse the impact of real bubbles on the economies of Japan (1980-2009) and China (2010-2024) and to identify the bubble state in the same nations. Further, it was identified that there were no bubble crises in China in the year 2010-2024 due to Covid-19 pandemic. This research provides a recommendation for future researchers to work on other sectors apart from real estate and can involve new variables in their research, including demographic factors.

The objective of the study has been discussed below:

• To examine the 1990 Japanese real estate bubble crisis.

• To examine the post-pandemic real estate bubble crisis in China.

• To analyze the impact of the real estate bubble crises in Japan in 1990 and post-pandemic real estate bubble crises in China on Economic growth.

2. Literature Review

The financial industry is interconnected with the real estate market, including research on the stock market and credit. It is analyzed Japan's stock market and real estate market's relationship using time-series analysis to explore the factors impacting land price increases [3]. Similarly, this study states that the loan growth rate in the earlier period initiated an increase in land prices compared with the loan growth rate [4].

2.1. Cause of Real Estate Bubbles

It is discussed that the agency problem can be the cause of asset bubbles, and the consumer expectations for the future state of credit can also be the reasons for the deepening of the bubble [5]. Zhenliang and Shihe have identified the reasons for the bubble, such as speculation, expectations, irrationality, virtual capital, etc. [6]. The results depicted that the property price will increase a bubble when the elasticity of the supply is more than the elasticity of demand. Some relevant variables have been chosen based on the extensive literature that influences the real estate market's supply and demand. These variables have been summarised below:

2.1.1. Real estate bubbles

The real estate bubble refers to the increased market price of the real estate sector that differs from the market base price. It results in less prosperity in the economy and denotes the soaring land prices, due to which demand fell sharply.

The hypothesis can be explained as follows:

H1: The Japanese 1990 economic turmoil negatively impacts the real estate bubbles or pricing.

H2: COVID-19 in China has had a significant positive impact on real estate bubbles and pricing.

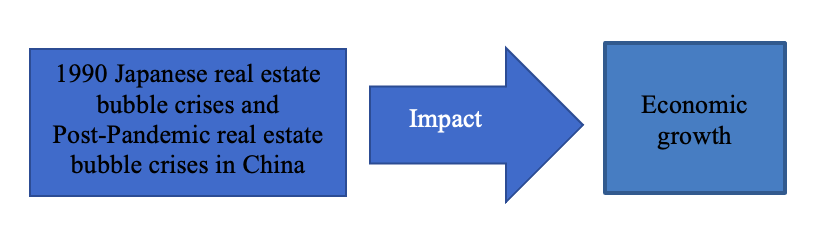

Figure 1: Conceptual Model

Notes: Impact of real estate bubbles in Japan and China oneconomic growth

(Source: Author’s calculation)

2.1.2. Covid-19 Pandemic

The Covid-19 pandemic did not disrupt the real estate market as most people were involved in digital or online-based transactions. The COVID-19 pandemic has changed market functioning by using new applications [7].

The hypothesis can be explained as follows:

H3: The effect of China's COVID-19 on real estate bubbles or pricing differs greatly from that of Japan's economic unrest in 1990.

Gross domestic product (GDP), Per capita

In general, a rise in GDP indicates the development and progress of the country and a rise in the supply of commercial real estate. The foundation of economic prosperity is spending and investment in the economy, which are stimulated by the growth of the real estate sector, which in turn builds household wealth and creditworthiness [8]. Conversely, a real estate recession results in a decrease in spending and investment, which is detrimental to the growth of the economy [9].

Inflation (Consumer Price-Index-CPI)

Variations in shelter costs have an impact on the inflation measurement. In American cities, rent as a percentage of the Consumer Price Index for all Urban Consumers (CPI-U) average for the previous year was 32%. Approximately 8% of the rent was paid by tenants for their principal residence, and the other 24% was designated as Owners' Equivalent Rent (OER) for owner-occupied dwellings.

Money supply

According to Cummings, supply is defined as the total amount of financial assets that are accessible inside an economy at a given moment. It involves the total amount of money in circulation, or the monetary base, as well as reserves balances, or the money that banks and other deposit-taking institutions have in their M1, M2, and Federal Reserve accounts. The study's conclusions demonstrate how an overabundance of money could cause inflation and have an impact on real estate investments because of rising discount rates.

Impact of Property taxes on housing prices

In general, buyers of real estate are more concerned with the purchase price, whereas investors are more concerned with the risk and potential returns on their investment. Previous research has shown how shifts in housing costs affect customers' psychological states and purchasing behaviours [10]. Additionally, a number of academics have examined how the property tax affects the economy and house prices; the general consensus is that the tax's implementation would result in a drop in housing values [11, 12].

The 2011 property tax was shown to have decreased the value of properties in Shanghai while simultaneously raising the value of homes in Chongqing in an opposite upward movement. This illustrates how regional cities' property prices differ from one another. Paying the property tax, which could have an impact on housing prices, is therefore the most crucial issue [13, 14]. Particularly, housing prices have been rising over the last fifteen years and have contributed to the growth in average wages.

Covid-19 and the commercial real estate industry

Prior studies have looked at how recessions impact the real estate sector, namely the residential markets. The markets for commercial real estate have been the subject of very few studies. Browne and Case, for instance, discovered that the office market was significantly impacted by the 1991 recession, which led to low rent and property prices. Numerous studies have examined the markets for actual commercial real estate. For instance, Rosenthal et al. discovered that the commercial rent gradient significantly flattened in cities that prioritised transit [15]. The market's future is affected by the change in the demand for commercial real estate, it is found.

2.2. Impact of Covid-19 on the different sectors of real estate

Construction companies in European regions were affected by the first wave of the Covid-19 epidemic, since their operational costs were found to be 25%-30% lower than their typical capability. In this period, there were strict lockdowns in the whole economy, causing labor deficiencies, supply chains, breakdowns, and shortages in construction materials. It motivates the health and security procedures which raises costs [13]. Afterwards, the businesses noticed that their security was superior to what it was during the first wave in the spring of 2020. In February 2020, the enterprises showed a 97.5% recovery from the pre-crisis level in their industrial area [16].

That time the V-shape of the whole construction sector emerged. The recovery can differ from state to state-based on the speed and intensity that occurred from the pandemic period on industries. The Covid-19 pandemic has badly affected the construction investment strategies and economic sectors.

2.3. Real estate market and stages of recession

The real estate market is an important asset for Chinese people, after the year 1998. In 2020, housing contributed almost 70% growth in household total assets among other assets. Financial investment includes almost 21.2% of a household’s total assets. Further, it was found that any changes in housing prices in China will contribute to a change in the household’s total wealth, and the application of the wealth effect may impact the household’s economic behavior. Chinese banks have issued, Wealth management products (WMPs) for regulatory arbitrage or window dressing [14]. It was found that the loan-to-deposit ratio was subject to strict regulations. Based on transaction-level statistics, it is argued that entrusted loans are essentially a market reaction to credit shortages.

The research presented here establishes China's economic cycle for the years 2012–2017. Furthermore, one stage was created by combining the stages of recession and depression. China's economic cycle from 2012 to 2017 can be divided into three phases: the recessionary period (2012–2013), the recovery period (2014–2015), and the overheating era (2016–2017). The burst of the real estate bubble could lead to a financial crisis. Numerous studies suggest that China is experiencing real estate bubbles, and these bubbles are continuously expanding. Previous studies found that the financial risks China is facing are mainly associated with real estate and China has gone through a complete economic cycle and experienced the craziest Carnival in real estate history in the year 2012-2017.

2.4. Government policies to control real estate bubbles in Japan

2.4.1. Zoning and the virtues of central planning

For construction plans and building codes, and zoning proposals in Japan, the central government is in charge, which are approved or rejected at the national level. In the event that there is a scarcity of affordable housing, the policy action plan is straightforward: build more in areas where people are eager to dwell.

2.4.2. Environmental efficiency

In the past 20 years, 20% of all high-magnitude earthquakes worldwide have struck Japan. These are the unpredicted situations that require careful planning and to development of armour buildings to tackle this threat. Japan can look on things to manage the economics of housing prices in such areas impacted by the climate change.

2.5. Government policies to control real estate bubbles in China

The Chinese government has made moves in recent years to tackle the crisis that occurred in the country's property sector. The new measures include the prices to be cut to the home buyers which is needed for a deposit and encouraging local authorities to purchase unsold properties.

3. Research Methodology

3.1. Data Collection

The entire set of information was gathered between 1980 and 2009 from the Housing Property Price Index for Japan and China, the total data was collected from the period 2010-2023. The Gross domestic product (GDP), per capita, CPI change (Inflation), Broad money (Money supply), COVID-19, and price bubbles are the key variables considered for the data analysis in the regression model. Covid-19 is considered as a dummy variable. The source is selected for data collection such as the World Bank website, and OECD websites for Japan and China.

3.2. Data analysis

For data analysis, descriptive statistics and correlation were conducted to develop an exploratory understanding of economic indicators and their relationship. A separate regression model has been developed for China and Japan to control the economic indicators (GDP, Inflation, and Money supply). The data analysis has been done using the software R Studio (Appendix A). For the data handling MS Excel 2019 has been used and its diagnosis of the robustness of the regression model, linearity assumption of the residual, homoscedasticity analysis, and multicollinearity analysis has been done. The variables such as Gross domestic product (GDP), Broad money (money supply), CPI change (Inflation), COVID-19 and price bubbles have been considered for data analysis.

4. Results and discussion

From 1980 to 2009, the average house property price index was 125 (SD = 20.32), which ranged from 93.85 to 166.31. However, the annual changes of HPPI are within -5.54% to 10.78%. During the period the average GDP annual growth was 2.09% and GDP per Capita growth was 1.75%. The average annual inflation in Japan from 1980 to 2009 was 1.16% ranging from -1.35% to 7.78%. The average annual broad money growth was 4.26% per year. Whereas in China during 2010 to 2024, the average HPPI was 114.93, where the average annual percentage change was 0.02% (LL: -0.03, UL: 0.11). In China, the average GDP per capita during this period was 6.39, and the average annual inflation was 2.25%, with an average money supply change of 11.75%. In terms of economic indicators during the chosen periods China has a stronger economic condition than Japan. In both countries inflation and GDP growth are moderately correlated (0.3 > r < 0.7), whereas, Broad Money (Money Supply) has a low and negative correlation with all other macro-economic indicators except Housing Price Index.

4.1. Historical Economic Matrices for Japan

The HPPI from the year 1980 to 1990 rose slowly. Moreover, in the year 1990, the HPPI was at its highest level and suddenly slowed down from the year 1990 to 2010. This result shows the sudden changes in prices; hence, it can be concluded that in Japan, there were real estate bubbles that impacted the GDP per capita. However, a sudden increase was found in HPPPI during the year 1980 to 1990 in Japan. Further, in the year, 1990, the HPPI was at its highest level. After the year 1990 to 2010, the HPPI gradually decreased in Japan which demonstrates the impact of macro-economic factors on the real estate market.

4.2. Historical Economic Matrices for China

A sudden increase in HPPI has been found during 2016, however, after 2019, no major changes have been found in HPPI. However, after 2019, the annual growth of HPPI became more stagnant than before, indicating no sign of a price bubble due to the COVID-19 period. There was a variation in HPPI from 2012 to 2016. Therefore, after the year 2016, a slight increase in HPPI can be found, and further, from 2016-2020, a stagnant line of HPPI can be observed, indicating no price bubbles in China.

4.3. Regression Model for Japan

Regression Equation for Japan:

Overall Effect = C1 + B1Year + B2Lost Decades

Controlled Effect = C1 + B1Year + B1GDPPC.PD + B2CPI.PD + B3BM.PD + B4Lost Decades

Year = Year of the recorded data

Lost Decades= Binary variable, where Lost Decades = 1 when Year is 1991 to 2001

GDPPC.PD = GDP Per Capita Percentage Difference from the previous year

CPI.PD = Consumer Price Index Percentage Difference from the previous year

BM.PD = Broad money or M3 (Money Supply) Percentage Difference from the previous year

Table 1: Regression Models for Japan

Dependent variable: | ||

HPPI | ||

Overall Effect | Controlled Effect | |

year | -1.036*** | -0.281 |

(0.306) | (0.562) | |

GDPPC.PD | 3.128** | |

(1.421) | ||

CPI.PD | -1.154 | |

(1.902) | ||

BM. PD | 0.984 | |

(0.690) | ||

Lost. Decade | 26.431*** | 31.398*** |

(5.503) | (5.606) | |

Constant | 2,183.323*** | 665.750 |

(610.808) | (1,126.412) | |

Observations | 30 | 30 |

R2 | 0.533 | 0.647 |

Adjusted R2 | 0.498 | 0.573 |

Residual Std. Error | 14.398 (df = 27) | 13.274 (df = 24) |

F Statistic | 15.382*** (df = 2; 27) | 8.791*** (df = 5; 24) |

Note: Outputs are based on the OLS method

Source: Author Calculations

*** Significant by 1 per cent level

** Significant by 5 per cent level

* Significant by 10 per cent level

In Table 1, as per the Model 1 of Japan, after controlling the trend of the year, Lost. Decade (1991-2001) (B = 26.431, p < 0.05) has been found to have a significant positive effect on the HPPI of Japan, even after controlling the other macroeconomic indicators in Model 2, Lost. Decade (B = 31.398, p < 0.01) showed an increased positive effect in HPPI. Besides, GDP Per Capita (B = 3.128, p < 0.05) has a significant positive effect on HPPI. However, annual inflation and money supply growth have no relationship with the price bubble. The model can predict 64.7% variability of the HPPI (F = 8.791, p < 0.05), which is statistically significant. The normality assumption is satisfied. However, a funnel structure can be found in the residual vs fitted plot, which shows the potentiality of Heteroscedasticity. Heteroscedasticity is the limitation of the model, and therefore, the model should be improved further to have a more credible understanding.

4.4. Regression Model for China

Regression Equation for China:

Overall Effect = C1 + B1Year + B2COVID19

Controlled Effect = C1 + B1Year + B1GDPP.PD + B2CPI.PD + B3BM.PD + B4COVID19

Year = Year of the recorded data

COVID-19 = A binary variable, where COVID19 = 1 when Year is more than 2019

GDPPC.PD = GDP Per Capita Percentage Difference from the previous year

CPI.PD = Consumer Price Index Percentage Difference from the previous year

BM.PD = Broad money or M3 (Money Supply) Percentage Difference from the previous year

Table 2: Regression Models for China

Dependent variable: | ||

HPPI | ||

Overall Effect | Controlled Effect | |

year | 3.698*** | 3.232*** |

(0.575) | (0.958) | |

GDPPC.PD | 1.259 | |

(0.739) | ||

CPI.PD | 3.820** | |

(1.261) | ||

BM. PD | -1.586* | |

(0.756) | ||

COVID19 | -2.246 | 5.035 |

(5.134) | (5.623) | |

Constant | -7,341.346*** | -6,400.976** |

(1,158.955) | (1,939.188) | |

Observations | 14 | 14 |

R2 | 0.898 | 0.959 |

Adjusted R2 | 0.879 | 0.934 |

Residual Std. Error | 5.381 (df = 11) | 3.976 (df = 8) |

F Statistic | 48.226*** (df = 2; 11) | 37.772*** (df = 5; 8) |

Note: Outputs are based on the OLS method

Source: Author Calculations

*** Significant by 1 per cent level

** Significant by 5 per cent level

* Significant by 10 per cent level

As per Model 1 of China HPPI, after controlling the trend of the year, COVID-19 (2020-2024) has been found to have no significant effect on the HPPI of China. Even after controlling the other macroeconomic indicators in Model 2, COVID-19 showed no independent effect on the HPPI of China. Besides, Inflation (B = 3.82, p < 0.05) has a significant positive effect size on HPPI, whereas money supply (B = -1.586, p < 0.05) has a significant negative effect on HPPI. GDP per Capita growth has no effect on the HPPI of China during the chosen period. The model can predict 95.9% variability of the HPPI (F = 37.772, p < 0.05), which is statistically significant.

5. Conclusion

This paper analyses the impact of the real estate bubble in Japan (1991-2001) and China (2020-2023) and findings suggest that China has a stronger economic condition than Japan. The housing price property index (HPPI) gradually decreased in Japan, demonstrating the impact of macroeconomic factors on the real estate market during the lost decades, where a significant drop has been found in annual changes in the HPPI growth rate. It supports the theory that shows both macro and micro-economic indicators affect the real-estate bubble. Furthermore, it is found that there is a significant effect of GDP per capita change on HPPI where the money supply and inflation did not have a strong effect on real estate bubbles in Japan. Hence, it can be said that the Japanese government should provide the possible measures to control GDP per capita change to control the price bubbles in Japan, which may impact the growth of the economy. However, for China, the direct impact of COVID-19 on HPPI is not significant, whereas the money supply has reductive, and inflation had an incremental effect on HPPI of China. It also indicates a potential indirect relationship between COVID-19 and changes in HPPI where money supply and GDP per Capita might play a mediator.

The findings of this research contribute to the real estate market, customers, and investors. The conceptual framework explains the relationship between real estate bubbles and economic growth while comparing the differences in the relationships in different economic settings (Japan and China). In terms of limitations, the two regression models (Japan and China) were developed using a linear relation. This research has not considered socio-economic factors such as age, gender, education, and occupation. This research has neglected other sectors such as retail, textile, and banking, so it recommends that future researchers work on the different sectors in the context of Japan and China.

References

[1]. Hong, T (2009) ‘Comparative study on the measurement and the causes of real estate bubbles in Japan and China’, B.E. (China University of Mining and Technology), Master of Economics in applied economics, Hunan University.

[2]. Myott HE (2000) ‘Developing and analyzing The Neighborhood Early Warning System’. In Hamline-Midway, Neighborhood Planning for Community Revitalization.127-156. https://www.forbes.com/advisor/mortgages/real-estate/will-housing-market-crash/

[3]. Takahashi, H and Terano, T (2003) ‘Agent-based approach to investors' behaviour and asset price fluctuation in financial markets’, Journal of artificial societies and social simulation, 6(3).

[4]. Wu, Y, Zhang, Y, Han, Z, Zhang, S, and Li, X (2022) ‘Examining the Planning Policies of Urban Villages Guided by China’s New-Type Urbanization: A Case Study of Hangzhou City’ International Journal of Environmental Research and Public Health, 19(24): 16596.

[5]. Allen, F and Carletti, E (2010) ‘An overview of the crisis: Causes, consequences, and solutions’, International Review of Finance, 10(1): 1-26.

[6]. Zhenliang, C and Fu Shihe (2000) ‘Real estate bubble and its prevention’, China Real Estate, (2): 7-11.

[7]. Bethune, ZA and Korinek, A (2020) ‘COVID-19 infection externalities: Trading off lives vs. livelihoods (No. w27009)’ National Bureau of Economic Research.

[8]. Miller, N, Peng, L, and Sklarz, M (2011) ‘House prices and economic growth’, The Journal of Real Estate Finance and Economics, 42: 522-541. DOI 10.1007/s11146-009-9197-8

[9]. Nneji, O, Brooks, C, and Ward, CW (2013) ‘House price dynamics and their reaction to macroeconomic changes’, Economic Modelling, 32: 172-178. http://dx.doi.org/10.1016/j.econmod.2013.02.007.

[10]. Surico, P and Trezzi, R (2019) ‘Consumer spending and property taxes’, Journal of the European Economic Association, 17(2): 606-649.

[11]. Kuang, W (2009) ‘Housing characteristics, property tax and house prices’, Economic Research Journal, 4: 15-22.

[12]. Zhang, P, Hou, Y, and Li, B (2021) ‘Impacts of Property Tax Levy on Housing Price and Rent: Theoretical Models and Simulation with Insights on the Timing of China Adopting the Property Tax’, China Finance and Economic Review, 10(3): 47-66.

[13]. Anderson, NB (2011) ‘No relief: Tax prices and property tax burdens’, Regional Science and Urban Economics, 41(6): 537-549.

[14]. Cai, M, Huang, X, and Zhao, D (2011) ‘Micro Analysis on Countercyclical Macro Regulation Policy Performance in Housing Market’, Econ. Res. J, 46: 80-89.

[15]. Chen, BK, Huang, SA and Ouyang, D (2018) ‘Can growing housing prices drive economic growth?’, China Economic Quarterly, 17(69.3): 212-235.

[16]. Huang, S, Chen, B, and Liu, Z (2012) ‘Rent-tax substitution, fiscal revenue and government real estate development strategy’. Econ. Res. J, 47: 93-106.

Cite this article

Zuo,J. (2025). A Comparative Study on the 1990 Japanese Real Estate Bubble Crises and the Post-pandemic Real Estate Bubble Crises in China . Advances in Economics, Management and Political Sciences,150,129-137.

Data availability

The datasets used and/or analyzed during the current study will be available from the authors upon reasonable request.

Disclaimer/Publisher's Note

The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of EWA Publishing and/or the editor(s). EWA Publishing and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

About volume

Volume title: Proceedings of the 3rd International Conference on Financial Technology and Business Analysis

© 2024 by the author(s). Licensee EWA Publishing, Oxford, UK. This article is an open access article distributed under the terms and

conditions of the Creative Commons Attribution (CC BY) license. Authors who

publish this series agree to the following terms:

1. Authors retain copyright and grant the series right of first publication with the work simultaneously licensed under a Creative Commons

Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this

series.

2. Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the series's published

version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial

publication in this series.

3. Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and

during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See

Open access policy for details).

References

[1]. Hong, T (2009) ‘Comparative study on the measurement and the causes of real estate bubbles in Japan and China’, B.E. (China University of Mining and Technology), Master of Economics in applied economics, Hunan University.

[2]. Myott HE (2000) ‘Developing and analyzing The Neighborhood Early Warning System’. In Hamline-Midway, Neighborhood Planning for Community Revitalization.127-156. https://www.forbes.com/advisor/mortgages/real-estate/will-housing-market-crash/

[3]. Takahashi, H and Terano, T (2003) ‘Agent-based approach to investors' behaviour and asset price fluctuation in financial markets’, Journal of artificial societies and social simulation, 6(3).

[4]. Wu, Y, Zhang, Y, Han, Z, Zhang, S, and Li, X (2022) ‘Examining the Planning Policies of Urban Villages Guided by China’s New-Type Urbanization: A Case Study of Hangzhou City’ International Journal of Environmental Research and Public Health, 19(24): 16596.

[5]. Allen, F and Carletti, E (2010) ‘An overview of the crisis: Causes, consequences, and solutions’, International Review of Finance, 10(1): 1-26.

[6]. Zhenliang, C and Fu Shihe (2000) ‘Real estate bubble and its prevention’, China Real Estate, (2): 7-11.

[7]. Bethune, ZA and Korinek, A (2020) ‘COVID-19 infection externalities: Trading off lives vs. livelihoods (No. w27009)’ National Bureau of Economic Research.

[8]. Miller, N, Peng, L, and Sklarz, M (2011) ‘House prices and economic growth’, The Journal of Real Estate Finance and Economics, 42: 522-541. DOI 10.1007/s11146-009-9197-8

[9]. Nneji, O, Brooks, C, and Ward, CW (2013) ‘House price dynamics and their reaction to macroeconomic changes’, Economic Modelling, 32: 172-178. http://dx.doi.org/10.1016/j.econmod.2013.02.007.

[10]. Surico, P and Trezzi, R (2019) ‘Consumer spending and property taxes’, Journal of the European Economic Association, 17(2): 606-649.

[11]. Kuang, W (2009) ‘Housing characteristics, property tax and house prices’, Economic Research Journal, 4: 15-22.

[12]. Zhang, P, Hou, Y, and Li, B (2021) ‘Impacts of Property Tax Levy on Housing Price and Rent: Theoretical Models and Simulation with Insights on the Timing of China Adopting the Property Tax’, China Finance and Economic Review, 10(3): 47-66.

[13]. Anderson, NB (2011) ‘No relief: Tax prices and property tax burdens’, Regional Science and Urban Economics, 41(6): 537-549.

[14]. Cai, M, Huang, X, and Zhao, D (2011) ‘Micro Analysis on Countercyclical Macro Regulation Policy Performance in Housing Market’, Econ. Res. J, 46: 80-89.

[15]. Chen, BK, Huang, SA and Ouyang, D (2018) ‘Can growing housing prices drive economic growth?’, China Economic Quarterly, 17(69.3): 212-235.

[16]. Huang, S, Chen, B, and Liu, Z (2012) ‘Rent-tax substitution, fiscal revenue and government real estate development strategy’. Econ. Res. J, 47: 93-106.